Monthly Market Overview - March 2026

Voluntary Biodiversity Market activity, trends, news, and developments.

Hi, Martin from bloomlabs here.

This is the third edition of the Monthly Market Overview based on our intelligence platform Bloom. It covers market activity, global trends, news, and developments from the Voluntary Biodiversity Market (VBM) across transactions, projects, organizations, headlines, and events.

For more in-depth VBM insights and access to Bloom data, sign up for free on the platform.

Disclaimer

Since the February edition, we engaged extensively with two of our data partners, Wilderlands and Le Printemps des Terres (LPDT), to clarify their data and ensure maximum accuracy.

We have integrated Wilderlands’ granular transaction listing of more than 5,500 items, which was previously a set of 5 aggregations. They now represent 81% of all transactions by count, and their all-time sales sum up to $1.8m, 34% of VBM value. Here are the restated monthly sales for the previous months: January 2026 hits $156k (previously $56k), and February 2026 increases to $42k (previously $20k).

We also received LPDT’s corrected data, previously identified as the 2nd developer by sales value with $1.7m. This number was inflated (and that was completely on us), and now sits around $630k. It brings the total VBM all-time value to $5.4m instead of $6.3m as stated in the previous edition.

Even though the market “loses” value from what we recorded before, I couldn’t be more satisfied to get closer to accurate numbers. Many thanks to our partners for helping us to cut through the fog.

If you have voluntary biodiversity credit transaction data, we want to hear from you. Suppliers who share data with us gain visibility on the Bloom platform, receive additional access to our market data, contribute to market transparency, and help build the pricing benchmarks very much needed. You can reach us at hello@bloomlabs.earth.

We are building the second version of Bloom, launching end of April / beginning of May. It will be much more intelligence-oriented and simpler to use regardless of one’s knowledge of the market. Until then, the data on the current version of Bloom will not be updated, so it will not match the figures in this article. We do apologize for the inconvenience.

Market context

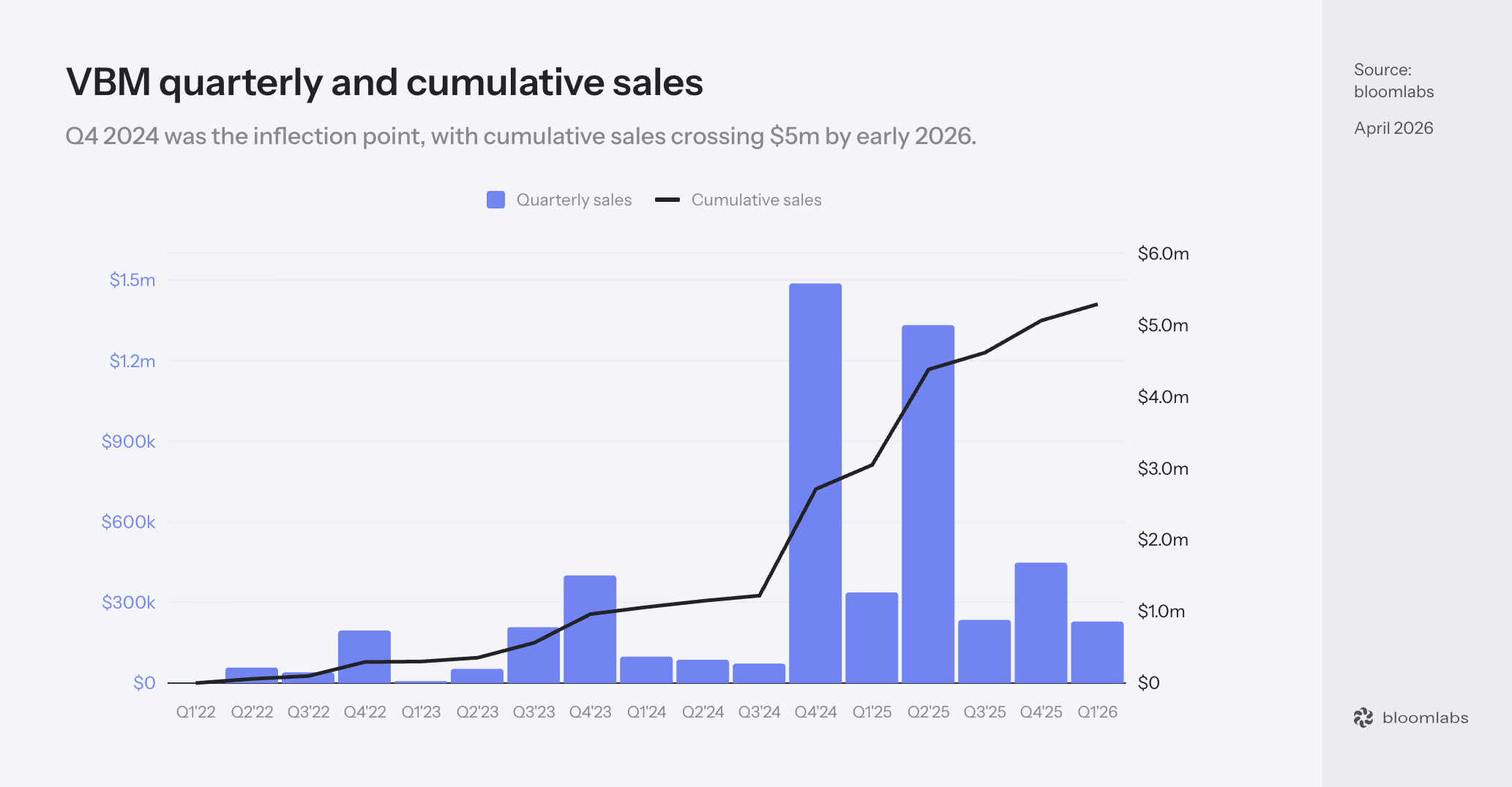

VBM has sold $5.4m worth of credits since the first recorded sale. However, we still believe a significant part happened over-the-counter (OTC) and has not been publicly announced yet. We maintain the estimate that actual total sales sit around $8m.

The year 2024 saw $1.7m in sales and 2025 recorded $2.4m. Q1 2026 closed at $229k across 242 transactions. Most other quarters land between $70k and $448k, so the beginning of the year is quite average, and is in fact the lowest quarter since the end of 2024.

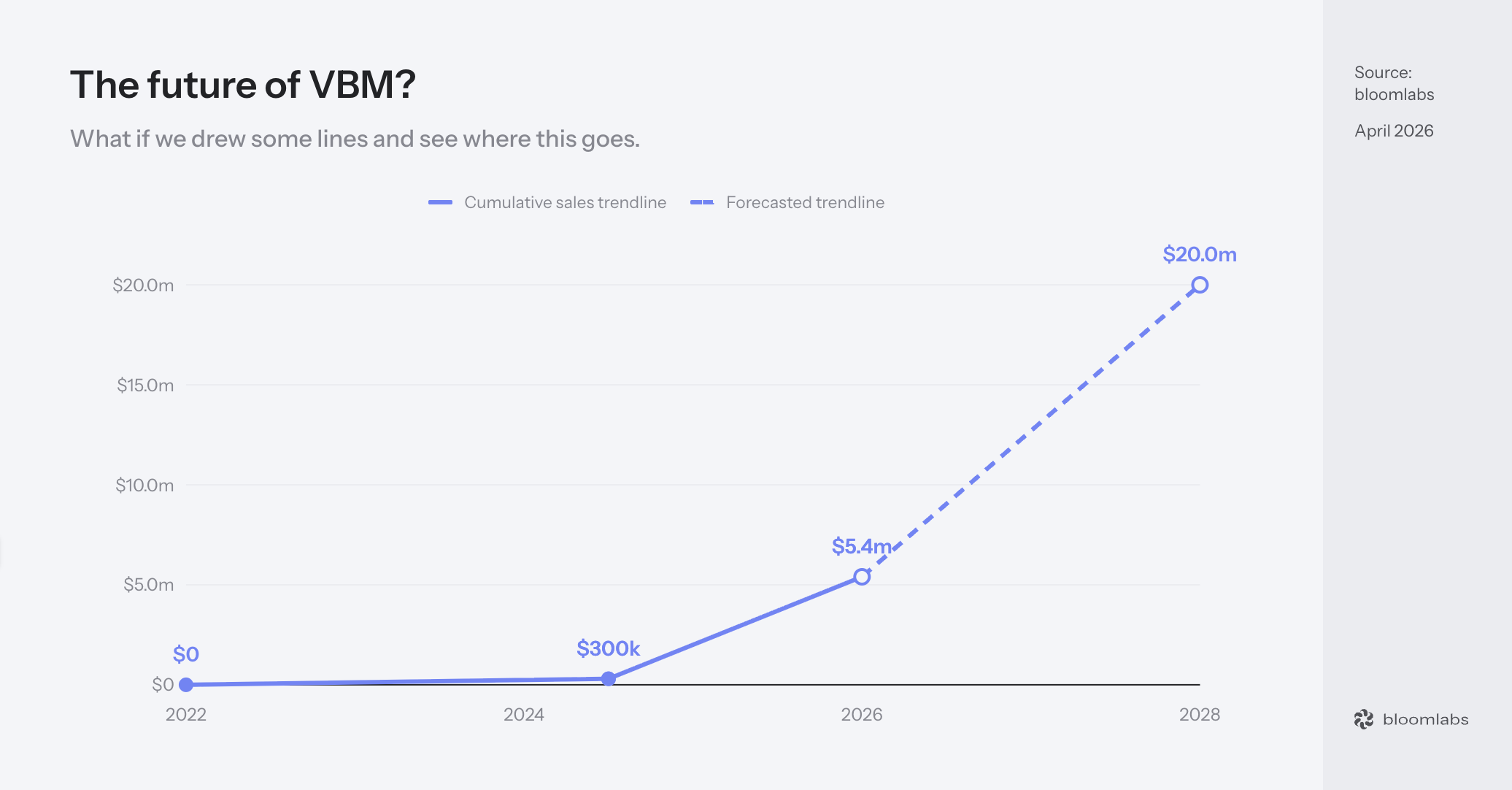

One could try to draw some lines from Q1 2022 to Q3 2024, then from Q3 2024 to Q1 2026, and infer that VBM is on an exponential curve. That’s not a game I want to play though, for we should only use data-backed assumptions. A lot of high-quality supply is coming to market in the next few years (Verra, Plan Vivo, CreditNature, Wallacea Trust, Cercarbono, etc), and this makes us confident that sales will increase. But without properly addressing the demand problem, a higher supply will not necessarily convert to higher sales, as we already see today with an estimated $50m credits stock unsold*.

We are not going to change the economic reality that companies seek profit. This is quite literally what they are built for, so either we accept it and we frame VBM in a way that accounts for it (building profitable investment opportunities, pushing for regulations and incentives, bundling credits to consumer products…), or we stay stuck in dependence on the philanthropic goodwill of a few organizations.

*This estimation should be treated with caution, since the exact volumes of credits issued and the credit price are still hard to obtain with precision for a significant portion of projects.

March 2026

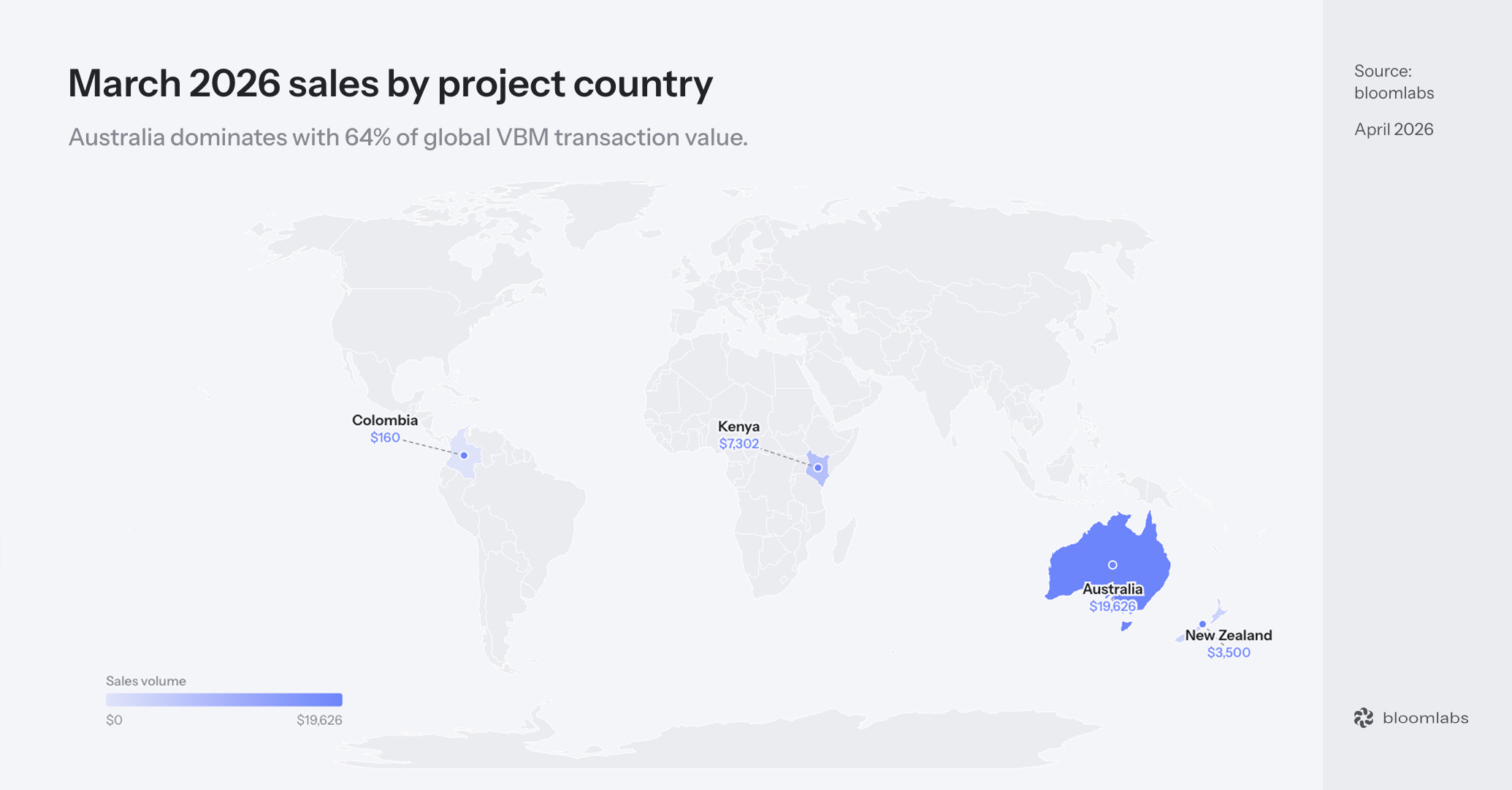

March 2026 saw $31k in total sales across 60 transactions, down from February’s $42k across 94 transactions and January’s $156k across 88 transactions. For perspective that’s one brand new car’s worth of credits sold in the world during 30 days, by all projects combined. The Q1 trajectory looks like a decline, but let’s remember that monthly comparisons in VBM are unreliable. Across all three months individually, the top 5 transactions consistently account for roughly 85% of total sales. Hence, a single $10k purchase landing in one month rather than another is enough to change everything.

Pricing

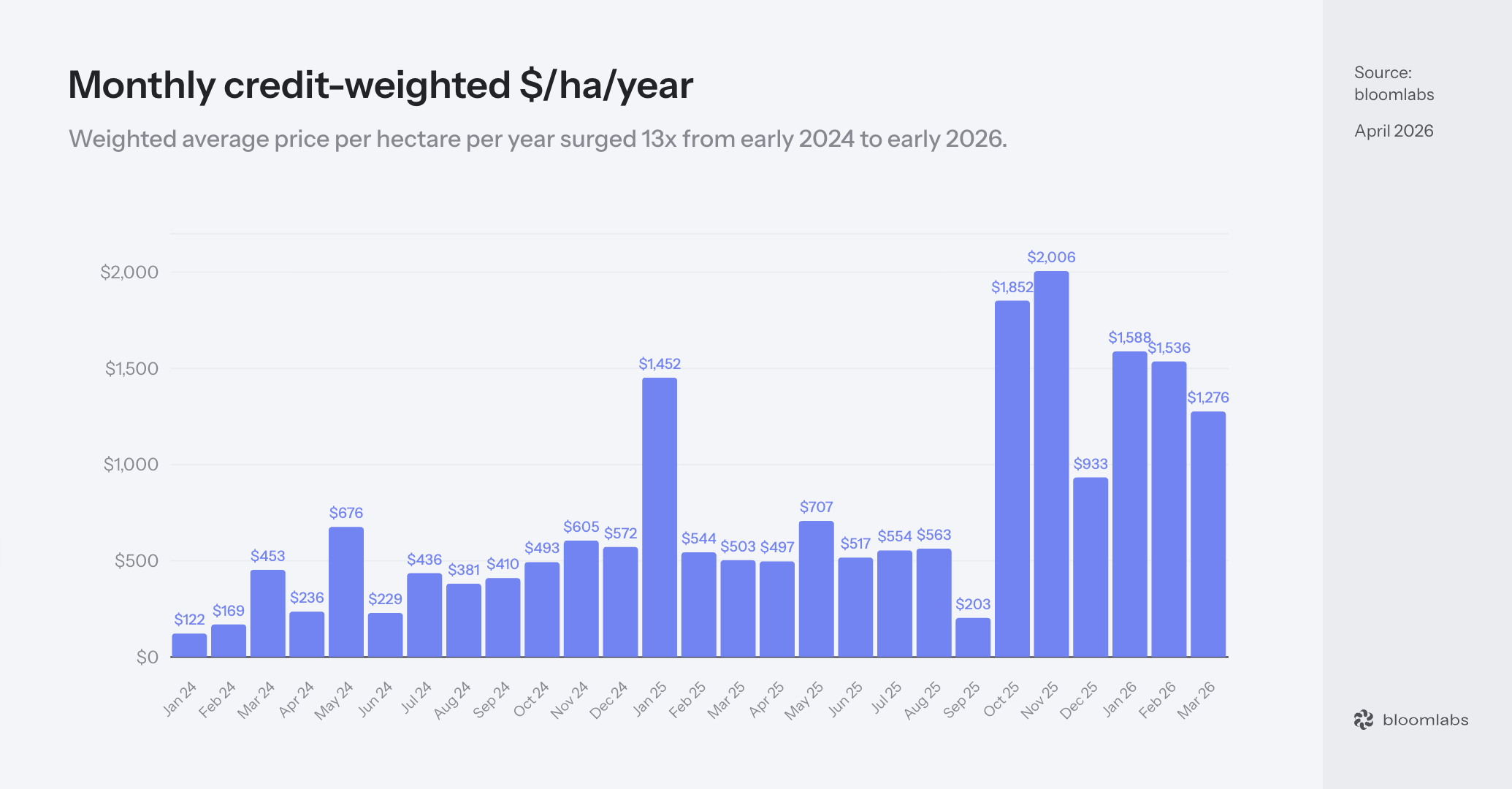

The $/ha/year indicator: Since the industry currently lacks a single, standardized credit unit, we use the price per hectare per year ($/ha/year). Every biodiversity credit transaction includes pricing, size, and duration parameters, making it the most efficient way to compare them so far and ensure relevance when analyzing different projects around the globe.

This month’s credit-weighted average $/ha/year reaches $1,276, the lowest in Q1. January was $1,588, February was $1,564. For reference, H1 2025 averaged $663 and H2 2025 averaged $1,032.

The drop comes from Wilderlands, for Coorong Lakes at $523/ha/year carries 54% of March’s sales weight, pulling the average down. Marereni at $3,000/ha/year counterbalances, but only represents 24% of this month’s sales.

Nothing systemic to overanalyze here, it mostly boils down to two project types with very different methodologies and pricing: a mangrove uplift credit in Kenya and an avoided loss credit on Australian shrubland are not the same product. Different ecosystems, different activities, different geographies, different cost structures.

The $/ha/year increase between 2024 and 2025 (with the beginning of 2026) is entirely due to Marereni credits sales from its developer Seatrees, which began in October 2025 (we can clearly see the effect on the chart). A good narrative could be that buyers are interested in more expensive projects, hence forecasting an increase in demand quality, but that is simply not provable yet.

Projects

Wilderlands quite simply dominated March with four projects, 39 transactions, $19,626 total, 64% of the month’s sales. Coorong Lakes alone accounted for 54%, driven by one anonymous $16,495 purchase (3,154 credits). All Wilderlands’ projects are Australian, terrestrial, and primarily Avoided Loss (prevention of biodiversity decline through project interventions such as preservation or land designation, in areas facing demonstrable and imminent threats).

Marereni followed on its steady course with 13 transactions, $7,302, mangrove uplift at $3/credit. The split was 5 B2B transactions summing up to $6,423 and 8 B2C purchases for $879. Marereni is the most consistent non-Wilderlands project in Q1 and sells every month. This is an achievement that very few developers can claim today.

Sanctuary Mountain Maungatautari recorded a single $3,500 B2B purchase from Moneyworks.

Buyers

More than 60% of March sales have no buyer enrichment, which limits buyer analysis for the majority of the month’s activity. The transactions that we know are B2B account for 91% of sales with known channel, consistent with January (96%) and February (94%), which both have been recalculated following the changes mentioned in the disclaimer.

Only one named buyer appears in March, Moneyworks, a small New Zealand financial services firm. The company is an NZ firm buying from an NZ project, following on the “local buyer, local project” pattern from February (and from the beginning of VBM).

This structural pattern has not changed, as small, locally anchored businesses buy from nearby projects. These are not large corporates making strategic biodiversity commitments under disclosure pressures or incentives. For the market to reach meaningful scale, it needs intentional B2B purchases from companies engaging with biodiversity as a material business risk, or at least a business case.

If you are exploring whether and how biodiversity credits fit into your organization’s strategy, we would love to talk. Reach out at hello@bloomlabs.earth.

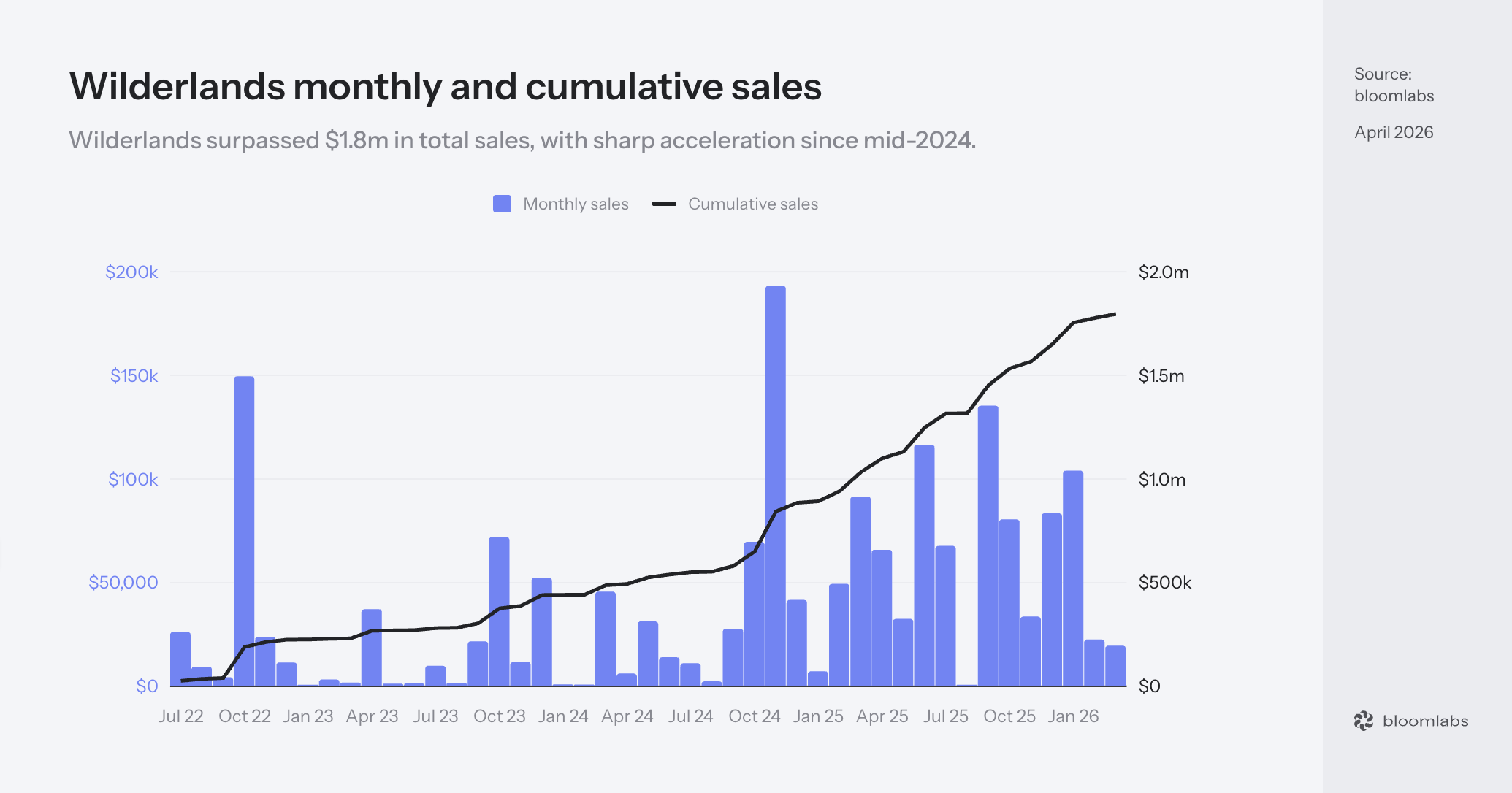

Wilderlands case study

Wilderlands strategy, being VBM’s largest actor by volume ($1.8m in all-time sales), can provide some sales insights.

They designed a clear unit that represents 1 square metre of protected land for 100 years, priced between $2 and $7. Simple enough for anyone to understand and cheap enough for anyone to buy. Thanks to that, they accumulate thousands of sub-$50 purchases (90% of their transactions) that prove demand exists and can be used to attract bigger fish.

Speaking of them, the 51 transactions above $10k generate 76% of their sales. Wilderlands has a true commercial approach to selling their credits. They partnered with Adelaide Festival two years in a row to protect habitat in the Coorong Lakes with $20k committed each time. They also partnered with al.ive body, an Australian personal care brand, which launched a limited edition product where each unit sold came bundled with a credit.

Wilderlands experiments with integrating its credits into existing purchasing decisions, and I find the al.ive body case particularly interesting. If a developer wants to sell 10,000 credits, it can either try to sell them to one company directly or it can partner with another that will bundle the credits to its products. In my opinion, the second path is worth exploring more and might be easier to implement, since the developer uses the company’s distribution, and the company uses the credits to increase the demand for its products.

Yes, an Australian company may have higher “goodwill” purchasing power than a Kenyan one. But the approach should be duplicable at each location’s own scale. I’m not on the ground trying to sell credits, so I may be disconnected from reality. But if so, I would be glad to hear some arguments as to why the Aussies’ system could not work everywhere else.

News

Featured

EU Expert Group on Nature Credits met in Brussels - March 20-21

My co-founder Simas attended the EU Commission’s 2nd Expert Group meeting on Nature Credits in Brussels on March 20-21. He published a full article with his takeaways and here is the tl;dr.

The Commission was well prepared and the amount of resources allocated to this project is serious. Five workstreams were discussed (methodologies and metrics, governance and integrity, market readiness and finance, policy coherence, international cooperation), each with a detailed concept note.

One of the most interesting design elements is the two-step certificate-credit lifecycle. The Roadmap is exploring how certificates could unlock upfront capital before full biodiversity results are in, and transforming them into credits once the outcomes are verified.

Demand-side representatives were however missing. The discussions were led by integrity providers, standard administrators, and project developers. Simas made the point clearly: if we expect nature credits to have impact at scale, “supply is only high-integrity if it is used”. Designing the system without the companies expected to buy credits, and then hoping they will participate once the infrastructure is set up is simply not realistic.

The key open questions are whether the Commission will pursue a purely voluntary model or move toward hybrid/compliance mechanisms, what the credit unit will look like (ecosystem condition seems to be the leading candidate), and at what scale the market will operate (local, national, or EU-wide).

National news

Germany proposes “Naturgutschriften” in federal law reform - March 31

On March 31, the German federal government published a draft law reforming the nature conservation intervention regulation (Eingriffsregelung) with a new section 16b in the Federal Nature Conservation Act. The reform introduces “Naturgutschriften” (nature credits) for the first time in federal legislation, creating a legal basis for voluntary private-sector investment in nature restoration beyond mandatory compensation obligations.

Trutz von der Trenck, co-founder of green account, shared: “For the first time, the concept of private-sector nature conservation is anchored directly in law. Through the introduction of nature credits, a bridge is created that we have long waited for: A legally secure basis for companies to invest massively in the restoration of our natural infrastructure, and specifically beyond mere legal obligation!”

Germany doing this at the federal level while simultaneously sitting on the EU Expert Group on Nature Credits tells me that national and EU-level market infrastructure are developing in parallel. This can be a great approach to experiment, iterate, and find solutions faster, which can then feed the EU’s regulations. Ideally every member state takes the same approach individually while building a common knowledge pool earned from practice.

Thailand launches national biodiversity credit roadmap - March 26

Thailand’s Biodiversity-Based Economy Development Office (BEDO) held a three-day workshop in Bangkok titled “Biodiversity Credit Roadmap of Thailand” with government, private sector, and international experts to study market mechanisms appropriate for the country’s ecosystems.

This makes Thailand one of the first Southeast Asian nations to develop a formal government-led biodiversity credit roadmap. Following the Philippines reef pilot covered last month, it is the second strong hint in two months that Southeast Asia is starting to seriously move.

Germany’s BfN launches research project on nature credits - March 18

On March 18, the Federal Agency for Nature Conservation (BfN) commissioned the Fair Finance Institute, in collaboration with the Institute for Ecological Economy Research (IOW) and NABU (an NGO we work with on the EU LIFE project), to conduct research on nature credit approaches and develop policy recommendations. The project will aggregate existing knowledge, interview stakeholders, monitor policy developments, and support BfN’s participation in European processes.

Two German federal initiatives on nature credits in the same month (the Naturgutschriften law and this research project) confirm that Germany is putting resources into building domestic market infrastructure for voluntary biodiversity credits.

Indonesia explores biodiversity credits for national park management - March 16

Indonesia’s Deputy Forestry Minister announced the government is exploring carbon trading and biodiversity credits to finance the management of its 57 national parks, currently funded entirely through the state budget. Way Kambas National Park is being prepared as a pilot project.

Indonesia’s national parks cover roughly 16 million hectares. If even a fraction of that enters biodiversity credit markets, the supply-side impact would be significant since Indonesia is one of the most biodiverse countries on earth.

Market news

Finnish landowners launch Luontoarvot nature values marketplace - March 27

MTK, Finland’s Central Union of Agricultural Producers and Forest Owners, launched the Luontoarvot marketplace to connect nature credit project developers with buyers. The platform, which received €500k in funding from Kone Foundation, currently lists 11 sites across Finnish forests. MTK is also a member of the EU Expert Group on Nature Credits.

Finland is joining the growing list of EU member states building domestic nature credit infrastructure. The landowner-led model is particularly relevant for Europe, where land is fragmented. According to MTK’s surveys, 80% of Finnish landowners consider protecting biodiversity important.

CDC Biodiversite and Removall partner on French national scheme credits - March 25

Removall, a carbon developer, announced an exclusive partnership with CDC Biodiversite to sell the first voluntary biodiversity certificates officially recognized by the French government, under the SNCRR programme (Natural Compensation, Restoration, and Renaturation Sites).

A carbon developer signing an exclusivity deal to sell nationally certified biodiversity credits is a strong hint that carbon market players see commercial value in biodiversity. The convergence between carbon and biodiversity I noted with Social Carbon last month is happening on the sales side as well.

To learn more about the links between those two markets, take a look at our Biodiversity and carbon credits in practice article.

Savimbo expands to Canada with InSight Biodiversity - March 20

Savimbo, the Colombia-based developer and one of the few with an actual track record of sales, is entering Canada. The expansion is led by InSight Biodiversity, a British Columbia-based team that will bring Savimbo’s ISBM methodology to Indigenous Communities and First Nations.

InSight Biodiversity is not looking to manage projects themselves, for their role is to act as a bridge between ISBM and communities by supporting the technical work, co-designing project management plans, and advising on certification and credit sales pathways. The funding and governance stay with the communities entirely.

Jake Raynard from InSight Biodiversity told me: “There is a growing movement here towards supporting conservation via Indigenous governance, for example with Indigenous Protected and Conserved Areas (IPCAs), so there is a good amount of government and philanthropic funding available for these projects. There’s also a recognition that there needs to be a movement away from reliance on grants though, towards a more self-sustaining financial model, and that’s where we are hoping to show that biodiversity credits can be one piece of the solution.”

Savimbo started in Colombia, built a methodology that works and sells, and is now exporting it. Drea Burbank, Savimbo’s founder, shared her vision with me: “We wanted a market, not a monopoly. The evidence is conclusive that fairness, standardization, inclusiveness, and interoperability are principles for scaling markets. We’re just following them.”

FSC publishes climate and biodiversity strategy (2026-2032) - March 10

The Forest Stewardship Council (FSC) published a new strategy that includes developing methodologies to measure and monetize ecosystem services, including biodiversity credit systems, and integrating them into its framework: “FSC will develop and integrate methodologies into its normative framework to measure and monetize impacts on ES, such as high-quality carbon or biodiversity credit systems, helping companies to meet regulatory requirements and voluntary targets.”

FSC’s size and reach in forestry certification is unmatched (173m hectares), but the majority of FSC certificate holders are productive forest owners. The organization sees biodiversity credits as an entry point for non-productive forest owners. The infrastructure (auditors, registries, chain of custody systems) already exists and could greatly facilitate credits adoption.

Cambridge tests Wallacea Trust methodology on UK sites - March 3

A University of Cambridge-led team tested the Wallacea Trust‘s biodiversity credit methodology on two English sites: a conventional arable farm in Lincolnshire (Boothby) and the Knepp estate in West Sussex, which has been rewilded for 20 years. They found that biodiversity at the conventional farm would increase by 69-92% after 30 years of restoration, worth an estimated GBP 1.5 million in voluntary biodiversity credits, but restoration costs would be roughly fifteen times higher.

They concluded that voluntary biodiversity credits alone will likely not fund nature recovery. They could work as complementary funding alongside carbon credits, public funding, payments for ecosystem services, and other revenue streams.

The Evenlode project last month made the same structural argument, in that biodiversity credits can be one layer in a blended finance stack, not the sole revenue source. That’s an interesting approach that I would love to see more of.

Suggested reads

Connecting nature, climate, and capital

Bank of New Zealand, Deloitte, and The Nature Conservancy published a joint report on nature finance. The demand curves they project are speculative given where VBM is today, but the core argument makes sense: the biggest demand driver will be mandatory corporate disclosures on nature, not voluntary contributions.

I would love to see more discussions around incentives alongside the regulatory-oriented ones. The carrot has what the stick lacks, in that it creates a system where everyone wins. Corporates win through, for example, tax benefits on biodiversity credit investments, and developers win by selling more credits. It bases the exchange on a positive relationship rather than an obligation, and could, in my opinion, favor deliberate quality procurement from companies.

50 investible opportunities for a new nature economy

The World Economic Forum, in collaboration with Oliver Wyman, published a report identifying over 50 investible opportunities that could generate up to $10.1 trillion in annual business revenues and cost savings by 2030. The report frames nature risk as a systemic economic risk and a missed commercial opportunity.

I agree with the framing and core message of the report, stating that businesses will transform their operations only if it makes economic sense, not because someone asked them to. VBM needs this framing to attract real money.

Upcoming events

April 22 - LIFE Biodiv CrEW webinar: biodiversity credits in European wetlands - online

We will host, alongside Eurosite, aeco, Sylva, NABU, and the European Landowners’ Organization (ELO), a joint webinar as part of the LIFE Biodiv CrEW project. Simas will present on biodiversity credits, schemes, and the market. ELO will cover project sourcing lessons, and Sylva will close on financial flows. This is the first public presentation of our LIFE benchmarking findings.

On a related note, our consortium members are engaging with companies that want to learn, test, and help shape this emerging market, including options for early participation. To learn more, contact Marc Maleika from Sylva at marc@sylva.earth.

April 27-30 - Environmental Markets Conference - US

Mitigation banking, carbon, water quality, and biodiversity markets. The US compliance mitigation market (over $6.2 billion) offers the most mature infrastructure lessons for VBM in terms of practically every market design aspect. Simas will attend and present. If you are at EMC and want to discuss biodiversity credit market intelligence, reach out to him at simas@bloomlabs.earth

May 4-8 - European Conference for Biodiversity Monitoring (BioMonWeek) - France

Inaugural edition of a planned biannual European conference on biodiversity monitoring, co-organized by Biodiversa+, GBIF, MARCO-BOLO, BioAgora, and Alliance for Nature. Nine thematic tracks will cover terrestrial, marine, and freshwater monitoring, data management, mass monitoring methods, policy, governance, and private sector cooperation.

I will attend the event and present the state of the market with a focus on monitoring, in partnership with Biotope, one of the leading European biodiversity consultancies. If you plan to attend and want to discuss, reach out to me at martin@bloomlabs.earth

May 11 - “Make Nature Count” seminar and workshop - Norway

Morning seminar at KPMG Oslo exploring how nature can be valued as an economic resource, organized by KPMG, Fossagrim, Gjensidige, and Belief Group. Speakers include Per Espen Stoknes (BI Center for Sustainability), Thina Saltvedt (Nordea Bank), and Dominik Maczik (BCA). The seminar will be followed by an afternoon workshop on building a high-integrity nature market in a European context.

I will attend the event and discuss the state of the market during the workshop. If you plan to attend or will be in Oslo around this day and want to discuss, reach out to me at martin@bloomlabs.earth

May 19 - “A Credit to Nature: A Matter of Interest” conference - Belgium

Organized by the Belgian Federal Council for Sustainable Development, with Wageningen University presenting on nature credit market development in the Netherlands, followed by a buyer use-case panel and a lunch marketplace for developers and funders. I love the idea of speed-dating between buyers and sellers, we need more of these.

June 3-4 - EU Green Week 2026 - Belgium

The 26th edition, organized by DG Environment, will be all about the business case for nature. The programme includes a startup-investor matchmaking event for nature-based solutions and nature-related technologies. Simas will attend the event and present the state of the market, so reach out to him at simas@bloomlabs.earth if you want to discuss.

July 14-16 - Global Nature Positive Summit - Japan

An international event to assess the current progress of the Global Biodiversity Framework, under the Japanese Ministry of Environment patronage. If you attend, please reach out to share your findings with us.

October 19-30 - CBD COP17 - Armenia

This is the single most important policy event for VBM in 2026. More details to come throughout the year.

| A guest post by

|