Monthly Market Overview - February 2026

Voluntary Biodiversity Market activity, trends, news, and developments.

February was a quiet month with $20k in sales across 5 projects. But the signals from policy and standard-setting were louder: IPBES published a landmark assessment linking nature loss to systemic economic risk, Social Carbon officially entered biodiversity certification, the Biodiversity Credit Alliance questioned the idea of a single fungible biodiversity credit unit, and Sweden publicly backed a voluntary approach for EU nature credits.

This article is the second edition of the Monthly Market Overview based on our intelligence platform Bloom. It covers market activity, global trends, news, and developments from the Voluntary Biodiversity Market (VBM) across transactions, projects, organizations, headlines, and events.

For more in-depth VBM insights and access to Bloom data, sign up for free on the platform.

Disclaimer

Starting with this edition, Niue Moana Mahu project and transactions are excluded from Bloom datasets. The project does not incorporate direct biodiversity measurements or independent third-party verification of ecological outcomes, and therefore does not meet the requirements for being considered as a biodiversity credit. This results in a restatement of cumulative sales.

We are currently drafting a standard of inclusion for what counts as a voluntary biodiversity credit, and what does not. This standard aims to be compatible with scientific rigor and market reality.

Market

Context

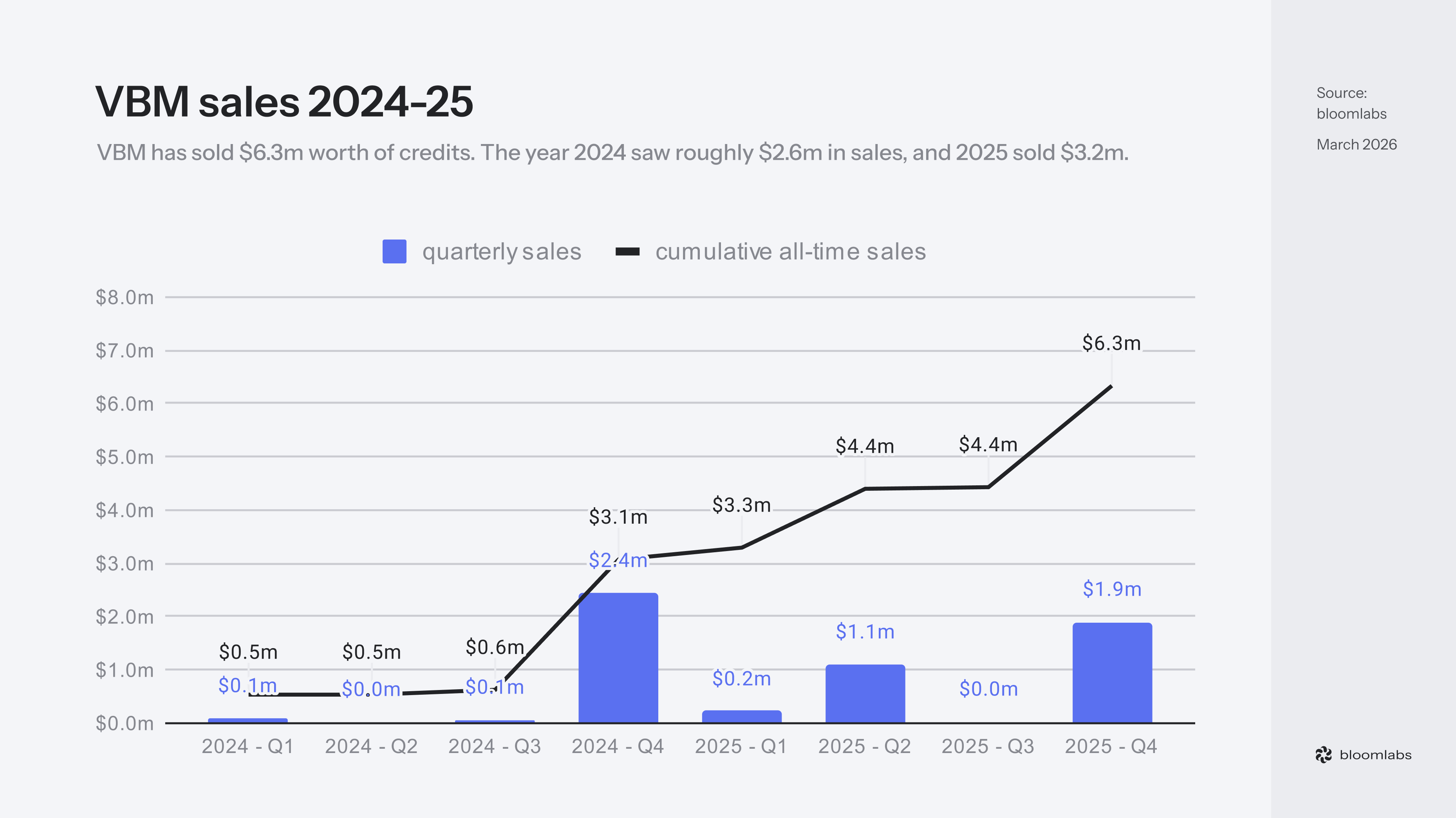

Adjusted for the Niue exclusion, VBM has sold $6.3m worth of credits since tracking began. However, a substantial part of VBM transactions happened over-the-counter (OTC) and have not been publicly announced yet. Hence, we believe the the actual total sales estimates to be around $10 million.

If you have voluntary biodiversity credit transaction data, we want to hear from you. Suppliers who share data with us gain visibility on the Bloom platform, receive additional access to our market data, contribute to the market transparency, and help build the pricing benchmarks the market needs to mature. You can reach us at hello@bloomlabs.earth.

The year 2024 saw roughly $2.6m in sales and 2025 sold $3.2m. Q1 2026 has recorded $76k through its first two months. Quarterly trends should be treated with caution: a $1.1m Wilderlands aggregate in Q4 2025 alone accounts for roughly a third of the year’s total.

February 2026

February 2026 saw $20k in total sales across 40 transactions and 5 projects, less than half of January’s $56k. Month-on-month comparisons remain volatile at this stage of the market, so the drop is not necessarily a signal. The average single transaction value dropped to $165, down from $900 in January, alongside the total transaction count (63 last month). Overall, February was not an active month, but not an outlier: 7 months in 2025 had less than $20k in total sales.

Pricing

The $/ha/year indicator

Since the industry currently lacks a single, standardized credit unit, we use the price per hectare per year ($/ha/year). Every biodiversity credit transaction includes pricing, size, and duration parameters, making it the most efficient way to compare them and ensure relevance when analyzing different projects around the globe.

This month’s weighted average $/ha/year reaches $2,770, pulled up by the Marereni and Iford projects. Iford reaches $9,800/ha/year, Marereni sits at $3,000/ha/year, El Globo at $1,250/ha/year, Putumayo at $120/ha/year, and Sanctuary Mountain Maungatautari at $7/ha/year - spread from $7 to $9,800 across five projects in a single month. For reference, H1 2025 averaged $1,153/ha/year and H2 2025 averaged $1,468/ha/year.

This variance reflects the fundamental heterogeneity of VBM. Different ecosystem types (mangroves, farmland, forests…), different project activity (uplift, maintenance…), different geographies, and different credit standards produce very different pricing. A mangrove restoration credit and a forest maintenance credit are not the same product, and can not be compared on their credit price.

Projects

The Marereni project continues to lead by volume and sales with 4,500 credits sold for $13.5k, although the exact number of transactions is unknown. Its strategy is built around cost-effective ($3) and small (1m2) mangrove restoration units, generating steady monthly sales through accessible price points.

Sanctuary Mountain Maungatautari was the most active project by transaction count, recording 22 individual transactions totaling $4.3k across 612 credits. At $7/ha/year, its pricing sits at the bottom of the range, in line with a maintenance model.

The month’s largest single transaction was a $1.3k B2B purchase by the British Transplantation Society on the Iford project, a UK-based farmland uplift project in the South Downs National Park developed by the South Downs National Park Authority and certified through Earthly. At $9,800/ha/year, Iford’s pricing shows the high cost of biodiversity uplift on small land parcels in a high-income country.

El Globo and Putumayo maintained their thin but consistent B2C-driven activity.

Buyers

The B2B share at 88% is consistent with January (90%). The bulk of Sanctuary Mountain Maungatautari 22 transactions was driven by a mix of New Zealand-based B2B buyers in travel, hospitality, and membership organizations (HQ Travel Group, Kimi Ora Resort, Tourism Industry NZ Trust), alongside a tail of smaller B2C purchases.

These are not large corporates making strategic biodiversity commitments. They are small-sized, locally anchored, consumer-facing businesses, likely motivated by their geographical proximity to the projects. The “local buyer buying local project” is a common theme found at all buyer size levels, a sign that VBM is not a truly international market yet.

This is valuable early demand, but for the market to reach meaningful scale, it needs to attract larger intentional B2B purchases from companies engaging with biodiversity as a material business risk. The IPBES assessment discussed later in this article could help accelerate that shift.

Projects

Over 50 farms in the North East Cotswold Farmer Cluster have formally begun work on the UK’s largest and most ambitious nature restoration programme. The Evenlode Landscape Recovery project will see farmers paid to work together to restore more than 3,000 hectares of habitat in Oxfordshire, Gloucestershire, and Warwickshire, aligned with existing food production, over 20 years.

The project operates under Defra’s Landscape Recovery scheme, one of the three pillars of England’s post-Brexit Environmental Land Management (ELM) system. Each participating farm commits 10-15% of its less productive land to wetland creation, riverside habitat restoration, and natural flood management. The rest continues as working farmland.

The blended finance model is what makes this project structurally interesting for VBM. The £100 million public funding from government provides the base layer, but the project is designed to stack multiple private revenue streams on top: Woodland Carbon Code credits, soil carbon credits, Biodiversity Net Gain (BNG) units, natural flood management offtake agreements, and voluntary biodiversity credits. The project has already secured its first flood management offtake and expects to generate 1 million carbon credits over its lifetime. For biodiversity credits, no specific methodology or standard has been publicly announced yet.

This is one of the most significant farmer-led landscape-scale projects to reach implementation in Europe, and the lesson for VBM is clear: biodiversity credits may not need to carry the full cost of restoration on their own. In a blended model, biodiversity credits become one revenue stream among several, stacked with carbon, water, or any other environmental asset. That changes the economics for project developers and could make biodiversity crediting viable in agricultural landscapes, where a single revenue stream might not cover the full costs.

Philippines reef-based nature credit pilot

France’s development agency announced a €1.5 million commitment to two innovative finance pilots for marine ecosystems, including a reef-based nature credit project in the Philippines. The pilot is one of the first marine-focused nature credit projects in Southeast Asia, a region where biodiversity credits have been virtually absent.

France holds significant overseas territories in the Indo-Pacific, including New Caledonia, French Polynesia, Wallis and Futuna, Reunion, and Mayotte. All its overseas territories combined contain nearly 10% of the world’s coral reef area. These reef-dependent economies make France the fourth-largest reef nation on earth, behind Indonesia, Australia, and the Philippines. AFD, which committed €736 million to biodiversity-related initiatives in 2022 alone and has been a major funder of marine protected areas, has a strategic interest in proving that credit-based models can work for reef ecosystems. If it works in the Philippines, it opens a financing template directly applicable to France’s own Indo-Pacific territories and AFD’s broader marine conservation portfolio.

This pilot extends VBM’s geographic reach into a region with high biodiversity value but almost no biodiversity credit infrastructure today. It also tests the feasibility of reef-based crediting, an ecosystem type that remains heavily underrepresented in VBM schemes, which still skew toward terrestrial habitats. Whether reef credits can be measured, verified, and sold in a scalable way is still an open question. This pilot is one of the first attempts to answer it.

Headlines

Social Carbon launches Nature Stewardship Framework

The scheme released its Nature Stewardship Framework (v1.0). The framework provides a structured and transparent way to assess whether conservation and restoration activities deliver meaningful, measurable change for ecosystems and the communities that depend on them, covering ecological, social, and institutional dimensions together.

This is a notable move from an established carbon standard into biodiversity certification territory. Social Carbon’s existing market infrastructure, registry, and network could accelerate adoption if the framework proves scientifically credible. It also signals that carbon and biodiversity standard-setting are converging as expected, a trend that project developers and buyers should watch closely. Verra with the SD Vista Nature Framework, Plan Vivo with PV Nature, and Cercarbono with the CBCP-01 methodology are a few other examples.

IPBES publishes landmark Business and Biodiversity assessment

IPBES published its Business and Biodiversity Report, approved on February 9th by representatives of more than 150 member governments during the 12th Plenary session in Manchester, UK. The assessment is the result of three years of work by 79 experts from 35 countries and synthesizes thousands of sources into a single integrated framework. Key figures include $7.3 trillion in global finance flows with directly negative impacts on nature in 2023 and a 40% reduction in natural capital stocks since 1992, while human-produced capital doubled over the same period. The report finds that biodiversity loss poses a systemic risk to economic stability, financial markets, and human wellbeing and proposes over 100 specific actions for businesses, governments, and financial actors.

Until now, the business case for biodiversity credits has relied heavily on voluntary contributions and philanthropy. The IPBES assessment changes the framing by stating at the highest intergovernmental scientific level that nature loss is a material business risk. It gives corporate decision makers a credible, citable basis for allocating budget to biodiversity, moving the topic from a CSR line item to a systemic financial exposure. And this type of exposure is the one that can motivate money flows.

If you are exploring whether and how biodiversity credits fit into your organization’s strategy, we would love to talk. Reach out at hello@bloomlabs.earth.

BCA releases discussion paper on biodiversity credit metrics

The Biodiversity Credit Alliance published Understanding Biodiversity Credit Metrics: A Business Imperative, a discussion paper aimed at helping businesses navigate the measurement landscape for biodiversity credits. The paper is structured around ten questions a business might ask before purchasing biodiversity credits, from “how are these different from carbon credits?” to “will AI resolve measurement uncertainty?”

BCA frames the absence of a single fungible biodiversity credit unit as a reflection of what biodiversity actually is: inherently diverse, locally specific, and impossible to compress into a biodiversity version of a CO2-equivalent. The paper points to equity markets, real estate, and consumer goods as examples of functioning markets that price heterogeneous assets without a universal unit. For buyers, the practical guidance centers on three steps: embed credits within a corporate nature strategy that applies the mitigation hierarchy, select credits aligned with the High-Level Principles, and ensure claims are transparent and proportionate to actual outcomes delivered.

If participants accept that biodiversity credits will remain heterogeneous, the question shifts from “how do we standardize a unit?” to “how do we make diverse credits comparable across their attributes, and selectable by use case?” BCA points to the latter direction, with an analogy to equity and real estate markets where assets are routinely priced across multiple non-standardized parameters.

We have shared our initial thoughts on biodiversity credit unit standardization in two earlier articles: Biodiversity Credits: Assets or Commodities? and Biodiversity Credit Calculation Overview: Version 2. The biodiversity credit unit conversation is crucial to the market development and we plan to cover more later this year as well.

Sweden backs voluntary approach for EU nature credits

Sweden pledged to support the development of a voluntary scheme for nature credits in the EU. The announcement aligns with the European Commission’s Nature Credits Roadmap, which foresees the expert group providing expertise on criteria and methodologies for nature credit markets by mid-2026 and governance frameworks by 2027.

This signals that at least one EU member state is actively pushing for the voluntary model within the Commission’s framework, rather than waiting for mandatory regulation. Sweden’s position reinforces the likelihood that voluntary biodiversity credits will have a recognized complementary role alongside EU regulatory tools.

We are part of the EU Commission Expert Group on Nature Credits and will be in Brussels later this month for the next working session. If you are working on nature credits in the EU and want to connect, reach out to us at hello@bloomlabs.earth.

Upcoming Events

March 4-6 - The Business of Conservation Conference in Nairobi

The Business of Conservation Conference returns to Nairobi, hosted by the African Leadership University’s School of Wildlife Conservation. This year’s edition focuses on changing the conservation narrative to one where conservation and development are aligned rather than opposed. Sub-themes include innovative sustainable financing for conservation (biodiversity credits, payment for ecosystem services, debt-for-nature swaps), community empowerment, the blue economy, and measuring biodiversity impact with technology and AI.

BCC is one of the few conferences that positions biodiversity finance within an African-led development framing rather than a European or North American policy lens. With the majority of VBM supply-side projects located in the Global South, events like this matter for connecting developers with buyer networks that reflect their context.

April 22 - LIFE Biodiv CrEW webinar: biodiversity credits in European wetlands

Eurosite, aeco, Sylva, NABU, the European Landowners’ Organization, and bloomlabs are hosting a joint webinar on April 22nd as part of the LIFE Biodiv CrEW project. The session will explore how biodiversity credits are being tested in European wetlands and what early implementation experience can teach about project design, eligibility requirements, and financial flows.

The agenda includes a presentation by Simas Gradeckas from bloomlabs on biodiversity credits, schemes and market, followed by ELO sharing lessons from sourcing biodiversity credit projects on the ground, and a closing session by Sylva on how the money flows.

On a related note, our consortium members are engaging with companies that want to learn, test, and help shape this emerging market, including options for early participation. To learn more or get involved, feel free to contact Marc Maleika from Sylva, marc@sylva.earth.

April 27-30 - Environmental Markets Conference in Chattanooga, TN

The Environmental Markets Conference brings together professionals across mitigation banking, carbon, water quality, and biodiversity markets in the US. The conference connects regulators, investors, environmental consultants, and corporate sustainability officers around conservation and restoration market infrastructure.

The US environmental mitigation market is decades ahead of the voluntary biodiversity market in terms of market infrastructure and volume. The lessons from wetland and stream mitigation banking on registry design, credit pricing, and buyer engagement are directly applicable to VBM as it matures. we will be presenting our work there, so if you are at EMC and want to discuss biodiversity credit market intelligence, reach out to us at hello@bloomlabs.earth.

Initiatives

Academic research on biodiversity credits in the Portuguese montado

Carla Janeiro from Universidade de Lisboa invites biodiversity credit project developers to contribute to an ongoing research initiative led by the University of Lisbon and the University of Evora. The project aims to develop a biodiversity credit mechanism tailored to the montado system, a traditional agro-silvo-pastoral landscape unique to the Iberian Peninsula. Input from practitioners is essential to ensure the research reflects real-world opportunities and challenges in voluntary biodiversity markets. If you are involved in biodiversity credit projects, your contribution would be valuable.

You can access the questionnaire here.

2026 State of Private Investment in Nature report

Forest Trends and NatureVest (The Nature Conservancy’s impact investment team) are partnering on the 2026 State of Private Investment in Nature report, the most comprehensive update of the nature investment landscape since 2016. The report will capture actual deployed capital, transaction-level performance data, capital efficiency insights, and analysis of which catalytic capital structures work to mobilize private investment across forestry, regenerative agriculture, biodiversity, water, carbon, and nature tech. All data is confidential and presented only in aggregated, anonymized form.

If you are a private investor, fund manager, or financial institution active in nature-based solutions, consider contributing to the survey. Respondents receive free early access to key insights and benchmarks. The survey closes April 15, 2026.

Upcoming from bloomlabs

We are working with key market participants to build the conditions for VBM to scale by providing extensive market intelligence. Our current focus is on understanding the demand side and the levers to unlock it.

Market Study on Scaling Biodiversity Markets with CDC Biodiversité

This study, commissioned by the European Investment Bank (EIB) and conducted together with CDC Biodiversité and the Mission économie de la biodiversité initiative, with the participation of bloomlabs, explores the demand for voluntary biodiversity certificates among French corporates and financial stakeholders, with the aim of informing EU-wide market design and policy recommendations.

The Nature of Demand with IAPB and WEF

This white paper is a strategic collaboration between IAPB, the World Economic Forum (WEF), and bloomlabs to publish a data-backed segmentation of buyer archetypes, which unpacks and contrasts current market action against market hesitation.

2026 Nature Markets Survey with Pollination Foundation

Jointly produced with Pollination Foundation, this survey will collect signals on market size, pricing, credit design, demand drivers, and rights-based participation to support a market snapshot covering the biennium 2024-2025.

| A guest post by

|