Takeaways from Brussels

Some impressions after a “nature credit week” in the Capital of Europe

Two weeks ago Martin and I attended the EU Commission’s 2nd Expert Group meeting on Nature Credits and the annual meeting of Biodiversity Credit Alliance (BCA).

It left us with our minds buzzing and a couple of takeaways:

Disclaimers:

1. Nothing written below represents the official views of the European Commission or BCA. Below are my thoughts about the EU Nature Credit Roadmap and the recent market developments. I’ve also avoided any specifics discussed in the meetings.

2. In this article, I used “biodiversity credits” and “nature credits” interchangeably.

3. The voluntary biodiversity market statistics below are powered by Bloom - our market intelligence platform.

Takeaways

There is progress

As much as one could wish for more speed, progress is here. Discussions that started at COP15 and led to the creation of BCA and the International Advisory Panel on Biodiversity Credits are now mulled over at the highest level in the EU. Key definitions, claims, use cases, legal status of nature credits and more are being clarified. Separately, the High-Level Principles (HLPs) are being operationalized.

That said, we are still deep in the policy-making phase. Naive me in 2023 would’ve expected a functioning market by now. It will take years before scale is reached with biodiversity credits outside of the few functioning markets.

The Commission was well-prepared

5 workstreams were discussed (meeting agenda):

Methodologies and Metrics

Governance and Integrity

Market Readiness and Finance

Policy Coherence

International Cooperation

Each workstream came with a well-researched concept note. They were good discussion starters. For those who found the concept notes too lengthy, I think more is better than less at this stage. “Throw stuff at the wall and see what sticks” is a proven strategy in reaching consensus. It also gave confidence that the Commission is allocating meaningful resources to the topic.

More importantly, the Commission was honest about the challenges and risks of nature credits and different design options.

Integrity and supply groups continue to lead market development

Throughout the week, the discussions were led by market integrity providers (standard administrators, market forums, NGOs and researchers) and credit project developers. Both are reflected in the market map here. It was also great to see the representatives of nature stewards: farmers, landowners, foresters and Indigenous Peoples.

We did miss the demand-side representatives though. Although the “high-integrity supply → high-integrity demand” thesis sounds great on paper, both sides have to develop at the same time.

If we expect nature credits to have impact at scale, I would argue that supply is only high-integrity if it is used. If so, high-integrity supply cannot be developed without the input of future demand.

The companies that are expected to buy these credits should share their opinion. I’m aware it’s more nuanced, with many of them being represented by lobby groups and other intermediaries. But to expect meaningful voluntary demand, their input needs to be considered. We can’t expect them to simply participate in the market once the infrastructure is set up.

Certificate-credit lifecycle: new design element

The two-step model (certificates → nature credits) mentioned in the Nature Credit Roadmap is a new design element, different from virtually all voluntary credit schemes. At first glance, it looks similar to the EU Regulation on Carbon Removals and Carbon Farming (CRCF) and their own two-step approach (certificates of compliance → certified units).

However, under CRCF, the certificate of compliance confirms that an activity has passed an audit. It does not seem to have a financial function. Instead, the Roadmap is exploring how certificates could build investor confidence and enable project developers to access payments before full results are in, since biodiversity outcomes usually take longer to materialize than carbon and can be less predictable.

Without deeper analysis, the certificate-credit model seems like an elegant way to tackle the upfront costs of conservation. I’m sure the devil will remain in the details.

Finally, I find it interesting that for nature, it is “nature credits” but for carbon, it is “certified units” when carbon is the one with a proven standardized unit. I’m sure I missed a fun discussion when it was decided in the carbon circles.

Key decisions to be made

The Roadmap has plenty of design decisions to make. Here are a couple I think about a lot:

Claims: contributions vs offsetting

Similar to the voluntary biodiversity market, the Commission has positioned contributions as the primary nature credit buyer claim category. The EU legal backlash against carbon-neutrality claims and related directives (e.g. Birds/Habitats/Water Frameworks) make offsetting seemingly unworkable. The contribution framing is intellectually (and legally) sound. It does create a weaker demand signal than the offset model though.

A lot will depend on the early market modeling results but I wouldn’t dismiss a scenario where a certain version of offsetting (or compensation/counterbalancing - whichever term you prefer) is explored. If that happens, the most straightforward scenario is a local-to-local like-for-like model, additional to any existing related regulations, as outlined in IAPB’s framework. A more ambitious scenario is the EU-wide biodiversity cap and trade system that BioInt’s Joshua Berger has been thinking about for some time.

Of course, biodiversity offsetting without regulations has proven to be unworkable integrity-wise. That leads me to the next design decision:

Legal regime: voluntary vs hybrid vs compliance

It is unclear whether the Commission will pursue regulation after the Roadmap is complete. Over-regulation is now a big topic in the EU and more justification is expected before sticks are introduced. Unsurprisingly, the Roadmap communication stuck to the voluntary framing.

That said, the Roadmap seems to follow the Better Regulation methodology. It is the same process the Commission uses to prepare legislative proposals. If we produce proof showing that voluntary demand cannot meaningfully close the EU biodiversity finance gap, the Commission would have political cover to propose harder measures in 2027.

So far, the data does not support the thesis that voluntary biodiversity credit demand will be enough with $6.4 million in total global sales over the past 4 years. Of course, the EU support and guidance would give a crucial credibility boost to the market. Still, given the evidence of other voluntary environmental markets, it is unlikely to play a meaningful role in bridging the €65 billion EU biodiversity financing gap.

So, unless we successfully link biodiversity credits to economic value (the north star of most nature finance geeks), we will need more direct incentives for corporates to buy beyond high-integrity contributions to nature. Carrots (e.g. tax benefits, lending incentives, procurement rules) and sticks (regulations, mandatory corporate reporting) will be required. Philanthropy and marketing, the dominant demand drivers now, cannot generate sufficient voluntary demand but they can play a part in ramping it up.

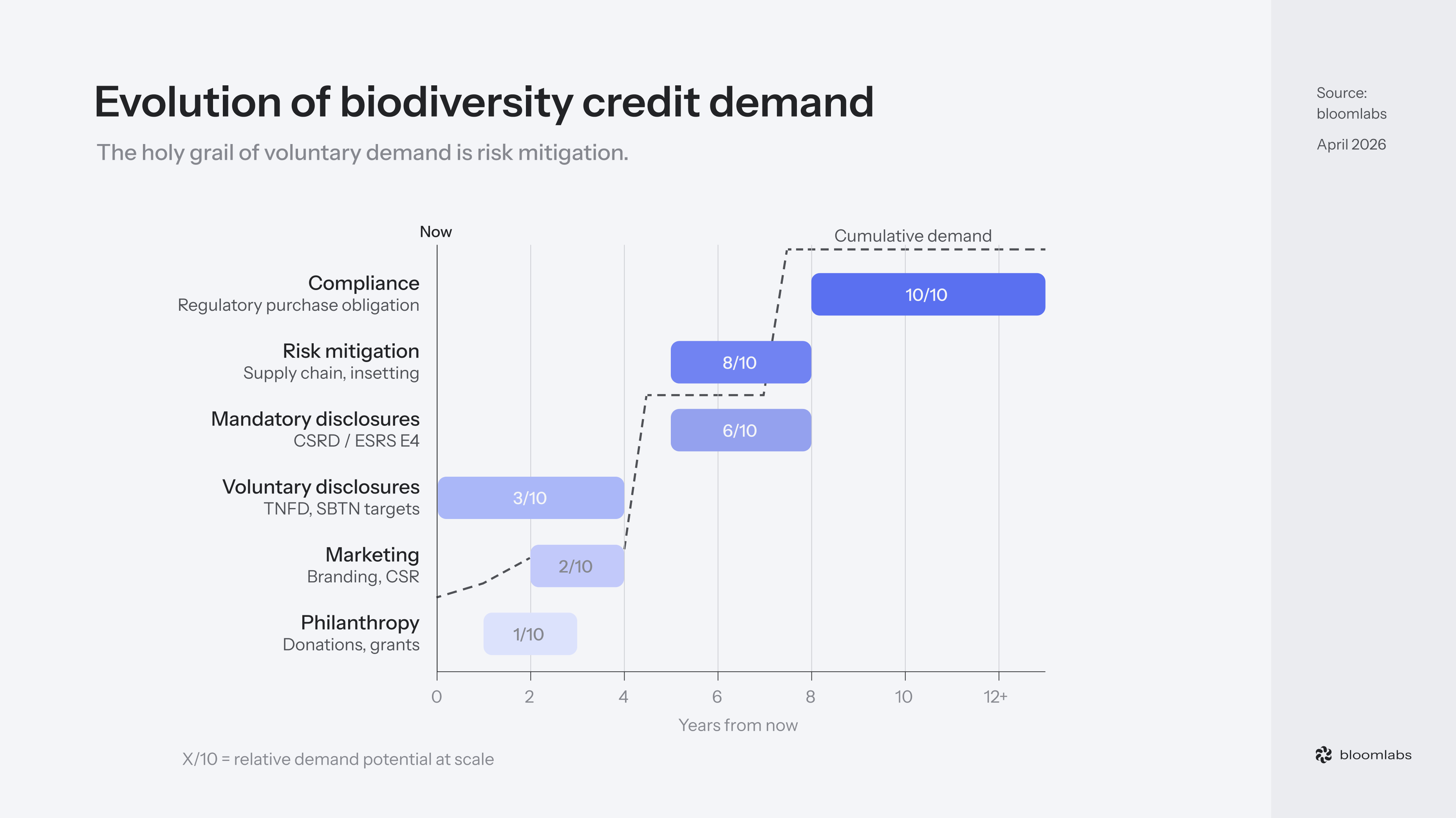

Here’s how the evolution of credit demand sources could look like:

It is a raw representation but the idea is that different credit demand drivers exist: different reasons, timelines and, most importantly, scales. The holy grail of voluntary demand is risk mitigation (if a market structure around it can be designed) while the compliance counterpart is a mandatory biodiversity credit market.

Every major biodiversity market has scaled through legal obligation. Germany’s eco-point system, England’s Biodiversity Net Gain, France’s compensation law and especially the US wetland and stream mitigation banking under the Clean Water Act - the largest functioning biodiversity credit market in the world.

An important detail: all these compliance markets were built around compensation. I’m aware that many nature credit market stakeholders are staunchly opposed to any form of biodiversity offsetting but these are the facts.

Scale: local vs national vs EU-wide

It is unclear at which scale the market would operate. From the perspective of volume and liquidity, a EU-wide market is the ideal. From the perspective of ecological integrity and current voluntary buyer patterns, local and national scales make more sense. A gradual bottom-up approach is also possible, starting from the least risky (local) and building towards a EU-wide market.

So far, voluntary biodiversity credit demand is hyper-local. Practically all B2B buyers (187) purchase credits from the country they are headquartered in: 96% in value and 99% in volume. France and New Zealand (the two largest B2B markets by sales) are completely domestic. Cross-border B2B purchases total just $144k across 16 transactions - less than 4% of the total B2B sales.

Credit unit and metrics: will there be any consensus at all?

This topic is still a big unknown. Ecosystem condition has become the unofficial backbone of voluntary biodiversity credit measurement. If the same happens for the EU nature credit measurement, one could assume that the credit (not certificate) unit might look something like “1 percent/point increase in ecosystem condition over 1 hectare for 30 years”. That’d be very close to the units of the well-known schemes such as CreditNature, Verra or Wallacea Trust.

One thing is certain - if a nature credit cannot be expressed in standardized physical terms (outcome, area, duration), it cannot function as a tradable commodity. The unit definition question alone can shape whether EU nature credits become a liquid, fungible market (or a set of markets) or develop into a custom project-finance instrument.

From our experience, using only biodiversity indicators (e.g. species richness, species diversity, habitat cover, etc.) for credit calculation and leaving out other indicators (e.g. socioeconomic, governance, etc.) as safeguards is the most reliable method to develop standardized units expressed in physical terms.

Tradability: yes or no

Tradability (or secondary markets) will likely vary in the certificate-credit lifecycle and will depend on credit type and geographic scale. However, if nature credits are based on ecosystem condition, that would create a base of a level of fungibility, and hence, tradability.

As always, secondary markets is both a big opportunity and risk. We expect to hear the well-known pro and against arguments. Pro: tradability is the only way to scale the market. Against: tradability is the path to lower ecological integrity, less efficient financial flows and harmful speculation.

Nature credits and carbon units: how will nature credits interface with CRCF?

No answers yet but the Commission is fully aware of the different ways the two could work together and is focused on ensuring clear links and boundaries between them.

Some argue that the nature credit roadmap shouldn’t have even existed and the biodiversity considerations should’ve been rolled into CRCF since the carbon market infrastructure is more mature. That’s an imperfect argument since not all natural ecosystems sequester carbon. CRCF is not designed for the conservation of inland freshwater ecosystems, grasslands or pollinator habitats in agricultural landscapes.

That said, I’m sure the Commission is aware of the market fragmentation risks by introducing another environmental credit.

Side notes

How do we not over-engineer?

As with most supply-led markets, there is a risk of designing a comprehensive, beautiful system that checks all the boxes.. but is not used. One way to avoid that is to include more end buyers in the market design. If we don’t include them, we shouldn’t kid ourselves - the only way to get them to buy credits is to enforce it through regulations. A voluntary system designed without the end buyers will simply not scale.

Ideally, we achieve elegance with a light set of guidelines that lead to the right outcomes instead of a prescriptive, polished but unusable framework. A couple of ideas:

1. We should admit what actually drives buyer activity: direct commercial benefits and simple compliance.

Indirect commercial benefits, such as philanthropy or marketing, have proven limited and unreliable in the voluntary carbon market. The same is true in the voluntary biodiversity market so far. I don’t expect that to change.

To start, the EU could provide early investor and buyer incentives to kickstart the market. Tax incentives, price floors, establishment of the EU nature credit buyers’ club or nature credit recognition in the EU Taxonomy are some examples.

2. We should not try to make nature credits the tool for all conservation.

As Sophus zu Ermgassen said, without strict guardrails of what a nature credit project is, it “very quickly degenerates into a system that generates almost no conservation benefits“.

There should be strict criteria for what projects are eligible to issue nature credits. The market is already over-supplied ($6.4m in sold credits vs an estimated ~$70.9m in unsold credits) with many more suppliers targeting the market. Additionality and transparent ways to verify it will become even more important in establishing which schemes/projects are considered high-integrity. As always with additionality, incentive management will be the challenge. Since it is easier to prove it for restoration, it is bound to fit the nature credit project activities best.

Two more cents: if we want nature credits to work, we should not get too creative. We should not try to imagine “what if corporates thought this way” or have the perfect answer to every single market design question. Instead, we should make the smallest set of market design decisions that minimize the blow-up risk (e.g. a catastrophic greenwashing scandal) and maximize learning. After a few years, we should reconvene and adjust. In other words, we should experiment more. As top-down as the EU regulations are, I believe that incrementalism is possible.

We don’t know what we don’t know. And even the things we should know from decades of nature credit market experience, we still often don’t.

My hope: the Commission ends the philosophical debates

Usually people disagree on the nature credit market design because they want it to be different things or don’t want it to exist at all. For those who support the market, most fall in the outcome-based philanthropy or full-stack financialization camps.

Unsurprisingly, since we’ve bet the farm on nature credits at bloomlabs, we believe that we can go beyond outcome-based philanthropy and form real markets in the EU and beyond the existing pockets elsewhere. The time is right: our ability to pull it off (technology, governance advances and, hopefully, political will) is meeting our need (undeniable and increasing economic effects of the nature crisis).

However, that is only possible with clear and consistent market rules. Usually, such rules are only established with the support of an influential organization. The Commission is in the perfect position to be that organization and set the precedent on how nature credits will operate in the EU and beyond.

That said, the Commission is under pressure to satisfy very different expert group stakeholders which often leads to agreeing on the lowest common denominator. And the lowest common denominator cannot be the most ambitious or productive. I hope the Commission doesn’t follow this approach and introduces data-backed opinions at the end of the Roadmap, even if that doesn’t please everyone.

Nature and EU competitiveness: how do we align them?

The common narrative is that regulations harm EU competitiveness. Since most of the EU sustainability policies are enforced through regulation, the same critique applies to nature conservation. As a big fan of EU-INC, this bothers me.

Being trained at startups, I’m used to the awkward silence once I tell my fellow tech bros what I do. The supportive will think I’m a “good guy doing philanthropy”. The cynical - that I’m a professional greenwashing enabler or a cog in a bureaucratic system that prevents the EU from competing with its gloves off.

There’s no denying that there is some conflict between nature conservation and competitiveness. Compliance costs are real and land use decisions are slower. Agricultural intensification and physical infrastructure development are major biodiversity loss drivers in the EU.

But the critique treats nature management as a cost and not critical infrastructure. That way, it’s easy to forget that all global economies completely rely on nature, including the EU. Statistical proof can be boring but here are a few of my favorites:

Degraded soils already cost the EU ~€40.9-72.7 billion/year (Panagos et al., 2025, via EEA).

That’s erosion, contamination, nutrient loss, compaction and sealing. And those estimates “may be around twice as high” because they exclude biodiversity loss, flooding and health effects.

75% of all corporate loans in the euro area go to companies critically dependent on nature (ECB, 2024).

Ecosystem degradation is a credit risk problem.

Timeframes explain the rest. Over five years, skipping infrastructure maintenance (i.e. nature conservation) might reduce costs. Over twenty, it might lead to full depletion and stranded assets. Can you imagine Europeans 100 years from now blaming us for focusing on nature too much instead of our competitiveness? The economic case for nature is much easier than the climate.

That said, I wonder if the Roadmap will experience deregulatory pushback or whether it will make a convincing case for why nature credits make sense for the EU economy in the short-term and not only the long-term (which is well-established).

Final notes

Again, I was impressed by the Commission’s preparation for the meeting. Thank you for taking the topic seriously. If I had to summarize the key challenges of the voluntary biodiversity market in two words, I’d say “demand” and “standardization”. Folks expect the Commission to deliver on both.

We are ready to support the Roadmap with our voluntary biodiversity market data and insights across our key credit scheme, transaction and credit project datasets on Bloom.

For others, the time to engage with the Commission is now. The market is being designed at this very moment. Companies that wait for the Roadmap outcomes to engage will find the options already narrowed.

Dear Simas,

thank you for this thorough report, very useful and insightful!

Your observation about demand-side voices being absent from the room is critical and too rarely said out loud. And your two-word summary : "demand" and "standardisation" is crucial to remember to make this work.

I applied to be in the group, but my remarks about the limitations for the voluntary biodiversity credit (demand remains stuck at $6.4 million over four years) isn't just a market design problem. It's a product problem. Biodiversity credits, sold as a standalone instrument, are structurally boutique: ecologically specific, illiquid, story-driven, and donor-adjacent.

That's not a criticism, it's the nature of the animal, so to speak, and that gives it its limits straight from the outset. No amount of EU Roadmap design elegance will push them through it.

The system I propose in https://www.arara.earth/ is treating biodiversity not as the primary credit, but as the integrity underwrite of a broader ecosystem performance instrument; a multi-aspect credit architecture with seven aspects: tracking alongside carbon and biodiversity, water, soil (health and carbon), air quality, cooling, and equity in a unified largely quantitative MRV-verified basket.

This change the design of an asset class completely. Water and cooling are the scalable yield drivers: every major corporation with supply chain exposure already prices water scarcity as a balance sheet risk, and tropical forest cooling through evapotranspiration represents arguably the largest unpriced ecosystem service on the planet. (my work is largely focused on saving the Amazon).

Carbon is the liquid on-ramp. Soil connects to regenerative agriculture capital. Equity, as Ostrom showed us, is a functional driver of ecological performance, not an SDG smuggled in.

Biodiversity sits at the center of this basket not as the volume product but as the quality certification layer. I see it more as the verified signal that the underlying ecosystem is healthy enough to make every other yield stream durable and investable. High biodiversity integrity equals investment-grade ecosystem. Degraded monoculture equals sub-investment grade, higher discount rate, shorter duration. The biodiversity aspect is what tells an institutional investor whether the water and cooling credits they're buying will still be performing in year 25.

Scientific research supports the value at scale: tropical forest ecosystem services (my expertise is in the tropics) are documented at roughly 5000 euro per hectare per year. A basket-based credit system capturing even a conservative 5–10% of that, creates something an institutional investor can actually underwrite. Stack verified, satellite-monitored, 30-year instruments across meaningful land area into a Special Purpose Vehicle, delivers the analogue of a nature bond, not a bespoke project-finance instrument dressed up in credit language.

I hope you can see this as an answer to the "demand" problem'' you rightfully flagged. You don't solve voluntary biodiversity demand by making biodiversity credits more elegant. You solve it by embedding biodiversity integrity inside an asset class that institutional and supply chain capital already has a reason to buy.

Your point about starting small and learning as you go makes sense. The EU's two-step approach of certifying first, trading later, is exactly the right way to build trust before the big money arrives. But the endpoint should be an ecosystem performance bond, not a biodiversity credit with better governance. This multi-faceted structure can close a meaningful share of the €65 billion gap. The latter, as the data shows, cannot.

The roadmap is still open. The time to engage is now. Do you know how I can get my voice heard? I am on the reserve list but I am hopeful my framework can bring a lot of value.

Thank you,

Rob de Laet