Monthly Market Overview - April 2026

Voluntary Biodiversity Market activity, trends, news, and developments.

Hi, Martin from bloomlabs here.

This is the 4th edition of the Monthly Market Overview based on our intelligence platform Bloom. It covers market activity, global trends, news, and developments from the Voluntary Biodiversity Market (VBM) across transactions, projects, organizations, headlines, and events.

For more in-depth VBM insights and access to Bloom data, sign up for free on the platform.

Disclaimer

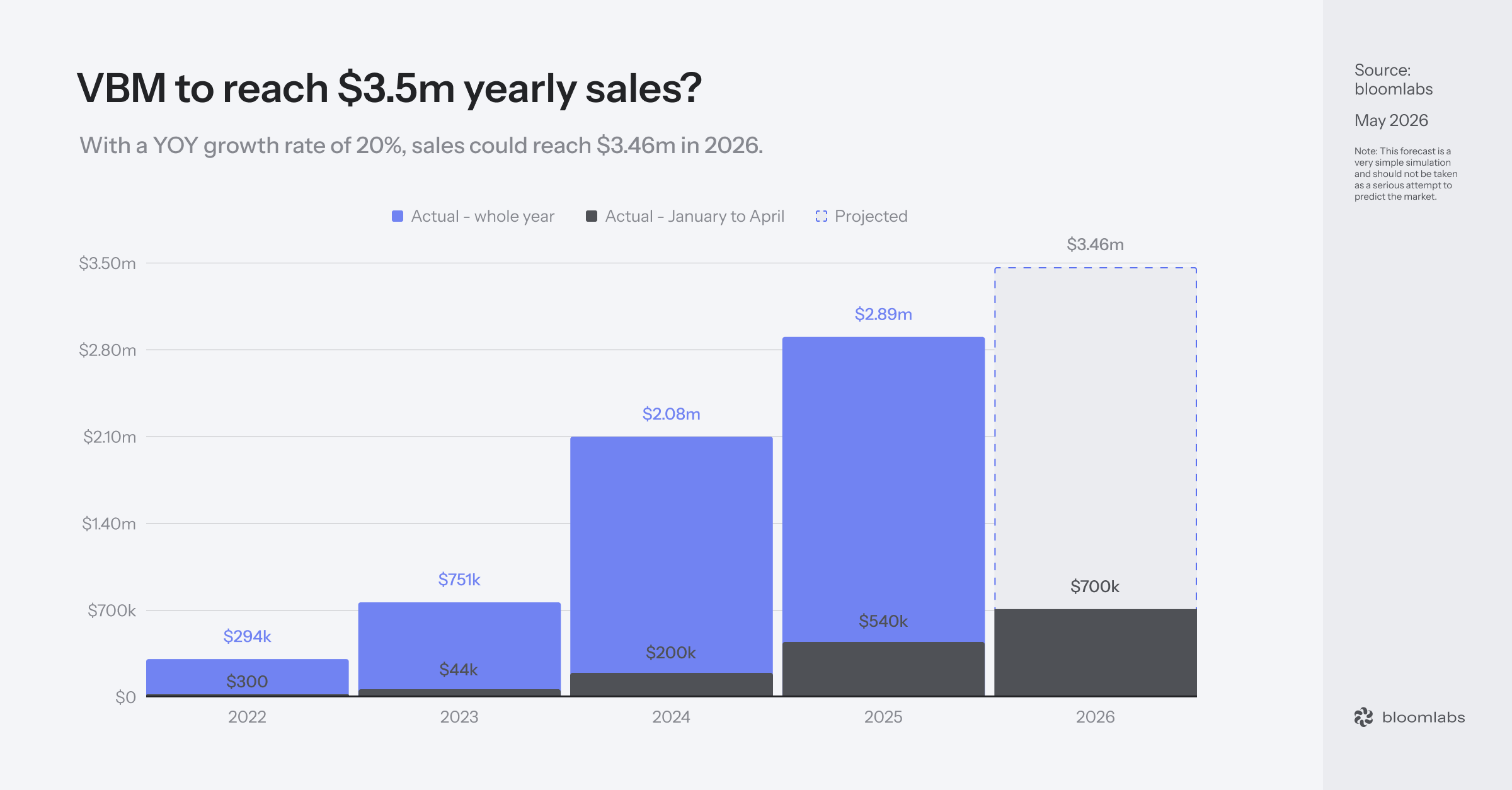

Since the March edition, we have integrated green account‘s transaction data into our database. green account is a German marketplace that sells biodiversity credits from German Eco-Points (Ökopunkte projects. This integration adds significant historical volume, with January now sitting at $307k (previously $156k), February at $48k (previously $42k), and March at $61k (previously $31k). The restated Q1 total is $416k instead of the $229k reported last month.

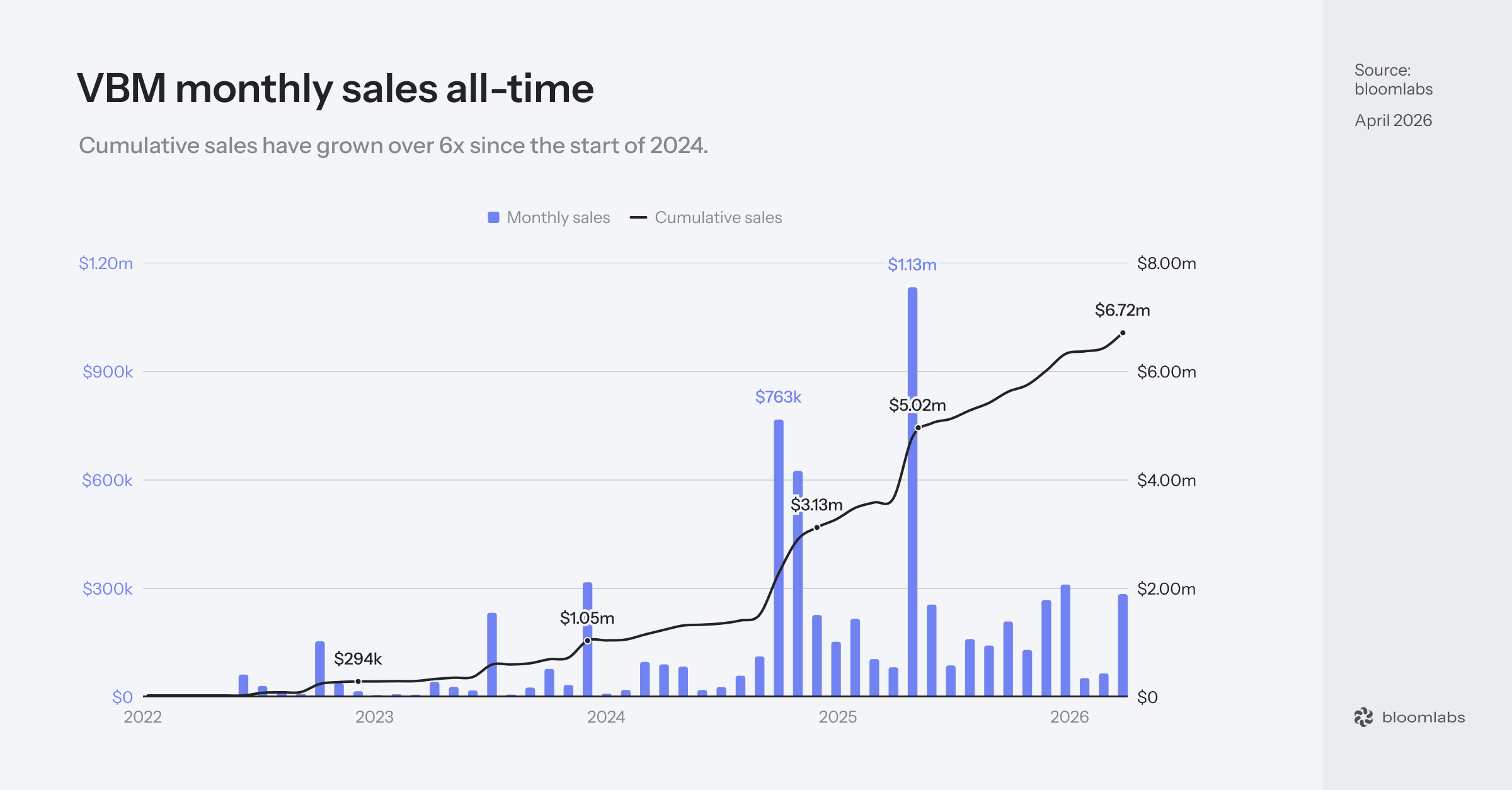

The yearly figures have also been updated, with 2024 now at $2.08m (previously $1.7m) and 2025 at $2.89m (previously $2.4m). The all-time cumulative VBM value through March 2026 is now $6.44m, up from the $5.4m stated in the previous edition.

This is the second consecutive month of significant data restatements, following Wilderlands and Le Printemps des Terres in March. I am glad the data keeps getting more accurate, and I understand the moving numbers can be frustrating for readers tracking month-over-month. But VBM data is still sparse and hard to obtain, and each data partnership brings a new layer of previously invisible transactions.

If you have voluntary biodiversity credit transaction data, we want to hear from you. Suppliers who share data with us gain visibility on the Bloom platform, receive additional access to our market data, contribute to market transparency, and help build the much-needed pricing benchmarks. You can reach us at hello@bloomlabs.earth.

We are launching the second version of Bloom, launching this month. It will be much more intelligence-oriented and simpler to use regardless of one’s knowledge of the market. Until then, the data on the current version of Bloom will not be updated, so it will not match the figures in this article. We do apologize for the inconvenience.

Market context

VBM has sold $6.72m worth of credits since the first recorded sale. We still believe a significant portion happened over-the-counter and has not been publicly announced, which would bring total sales to around $8-10m.

We have also recently found that approximately 10% of sales in the New South Wales Biodiversity Offset Scheme are voluntary, which would bring the total sales up by around $50m. We hope to share more details soon.

One pattern is becoming clearer with each month of data we collect. VBM sales are not on a steady growth trajectory but made of bursts of large B2B transactions surrounded by months of low-volume B2C activity. Month-on-month volatility is high, and the quarterly figures can move between $70k and $1.6m. Hence, monthly or quarterly comparisons don’t really make sense today.

April 2026

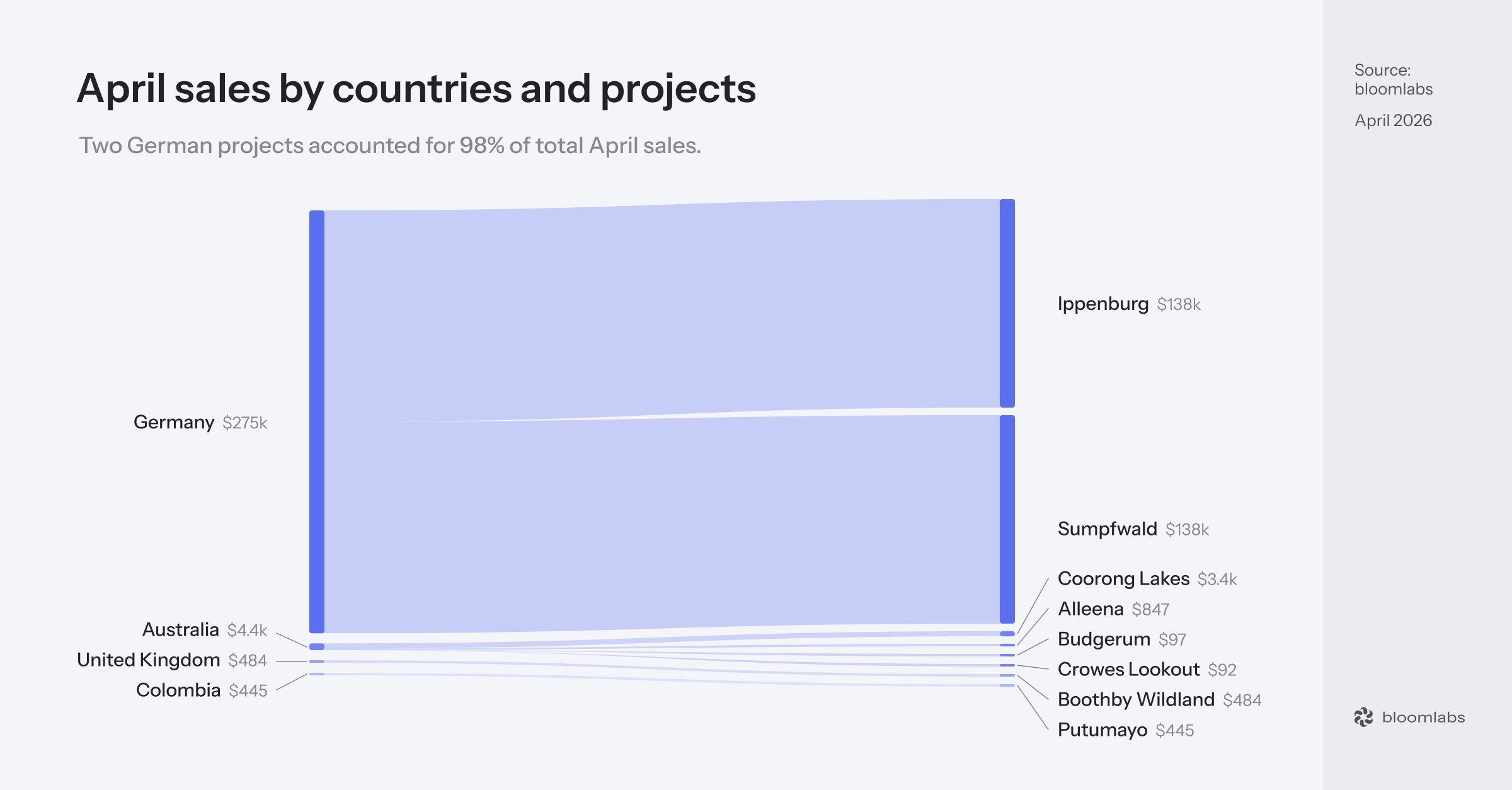

April 2026 recorded $280k in total sales across 47 transactions, up from March’s $61k across 62 transactions, February’s $48k across 95 transactions, and January’s $307k across 91 transactions. Two German projects account for $275k of that total, 98% of the month’s sales. April is the 6th biggest month for VBM since January 2022.

The top 5 transactions account for 98% of sales, the highest concentration in 2026 (January was 79%, February 82%, March 87%). But as mentioned earlier, monthly comparisons in VBM are unreliable, for a single large purchase landing in one month rather than another changes everything.

Projects

Ippenburg and Sumpfwald, two German projects sold through green account, topped April with a combined $275k (98% of the month).

Ippenburg is a 77-hectare ecological restoration project on the von dem Bussche family estate in Lower Saxony, restoring rivers, converting forests, and extending grasslands. Three B2B transactions from anonymous buyers generated $137k for 16,667 credits at $8.25 per credit. Sumpfwald is a 5-hectare wet forest conversion project near Düsseldorf, transforming a non-native poplar stand into a near-natural wet forest. One anonymous B2B transaction generated $137k for 25,000 credits at $5.50 per credit. Both projects are registered under the German Eco-Points system.

Wilderlands continued its steady B2C flow with its four projects (Coorong Lakes, Alleena, Budgerum, and Crowes Lookout) totaling 37 transactions and $4,394 in sales. Boothby Wildland recorded its first sale ever, a single $484 B2B transaction for 2 credits at $242 each. This is the 617-hectare Lincolnshire rewilding project developed by Nattergal and sold through the Earthly marketplace, more on them in the News section. Savimbo‘s Putumayo project in Colombia registered 5 transactions for $445, with 4 B2C purchases and 1 B2B transaction from EarthWin.

Buyers

B2B transactions accounted for 98% of April’s sales value ($275,850 across 6 transactions), while B2C made up the remaining 2% ($4,474 across 41 transactions).

The vast majority of April’s value has no buyer enrichment, since the four green account transactions ($275k) and the Wilderlands purchases are anonymous. The two named buyers that appear this month are both first-time purchasers, BHBIA and EarthWin.

BHBIA, the British Healthcare Business Intelligence Association, bought 2 credits from Boothby Wildland for $484. It is a UK-based professional membership organization for healthcare market researchers, headquartered in Sheffield. EarthWin, a US-based nonprofit focused on STEAM education and environmental awareness, bought 73 credits from Savimbo’s Putumayo project for $365 in a cross-border transaction (US buyer, Colombian project), which is rare enough to mention.

If you are exploring whether and how biodiversity credits fit into your organization’s strategy, we would love to talk. Reach out at hello@bloomlabs.earth.

green account case study

green account is a German marketplace founded in 2021 that connects landowners with companies investing in ecological restoration. They sell Ökopunkt, a government-defined biodiversity point that has existed since 1998 under the German Federal Nature Conservation Act. An accredited planning office assesses the biotope value of a given area before and after restoration on a standardized scale, the difference multiplied by the area in square meters gives the number of Ökopunkte generated, and the local nature conservation authority verifies the result.

The system was originally designed for mandatory compensation of construction impacts, and green account also operates a compliance marketplace (kompensationsmarkt.de) for that purpose. But the voluntary credits they sell are the same Ökopunkte, just retired with different motivations.

Four projects account for all voluntary sales, ranging from peatland rewetting (Moorprojekt, $563k) to multi-habitat restoration networks (Ippenburg, $432k, and Biotopkomplex, $267k) and wet forest conversion (Sumpfwald, $164k). All are Uplift (restoration) projects across four German states, all verified by local nature conservation authorities, and all B2B with anonymous buyers.

The Ökopunkte system has been running for almost 30 years, corporate buyers in Germany already know what it is from the compliance context, and the market infrastructure (planning offices, state registers, nature conservation authorities) already exists. green account just opened a voluntary channel on top of it. This is a much smaller ask than explaining the entire concept of biodiversity credits to a buyer who has never heard of them.

The $1.43m in all-time sales we track in Bloom covers only the voluntary side, since green account’s total transaction volume is much higher. Trutz von der Trenck, one of the company’s co-founders, confirmed that they facilitated nearly $24m on the compliance market.

Compliance markets can pull voluntary demand behind them, but the German case isn’t proof on its own. BNG in England or SNCRR in France don’t match the German performance to date. Something that might change in the hexagon (or baguette country for my non-French friends) with the partnership between Removall and CDC Biodiversité.

News

Featured

Barclays adds nature and biodiversity credit markets to sustainable finance framework - April 23

Barclays updated its Sustainable and Transition Finance Frameworks to include biodiversity criteria for the first time, developed with support from The Biodiversity Consultancy. Under the updated framework, financed activities must contribute to at least one GBF target and go beyond minimum legal requirements to mitigate or compensate for environmental harm.

A major bank naming nature credit markets as an eligible category in its $1 trillion sustainable finance framework is a strong signal. It could create a positive loop in which companies would buy biodiversity credits to access Barclays’ loans and investments. The voluntary biodiversity market today is almost entirely funded by small, locally motivated buyers (as we see every month in the transaction data), but any meaningful scale will come from institutional finance such as this one.

National news

Ethiopia includes biodiversity offsets in NBSAP - April 24

Ethiopia’s updated NBSAP, published on April 24, sets out how the country intends to raise ETB 87.4 billion ($557.8 million) by 2030 to finance its nature strategy, with biodiversity offsets and credits listed among the “innovative schemes” alongside payments for ecosystem services, green bonds, and benefit-sharing mechanisms. The NBSAP references Target 14 of the GBF with explicit language on requiring extractive industries, dams, and water infrastructure projects to apply biodiversity offset mechanisms.

Ethiopia is the first African country I’ve seen explicitly include biodiversity credits in its national strategy, and the compliance angle makes it particularly interesting. Most of the NBSAP language we track from other countries stays firmly in the voluntary space, but requiring specific sectors to offset their biodiversity impacts is a different proposition entirely. The US compliance mitigation market is valued at over $6.2 billion, and the English Biodiversity Net Gain approaches $450 million, proof that compliance generates volume.

Italy’s draft National Restoration Plan names biodiversity credits as a financing tool - April 24

Italy’s draft National Restoration Plan (NRP), open for consultation until June 9, explicitly names biodiversity credits alongside green bonds and payments for ecosystem services as innovative financing mechanisms to support the country’s obligations under the EU Nature Restoration Law (NRL). All EU member states must file a draft NRP by September 1, 2026, and a final version by September 2027.

The NRL requires 30% restoration of degraded habitats by 2030 and full coverage by 2050, and member states need to figure out how to finance it. If biodiversity credits become an accepted financing mechanism under national restoration plans, it creates demand that doesn’t depend on voluntary corporate goodwill but on governments needing to meet their own legal targets. A much stronger case, and typically one that creates entire markets. Since Member States have consistently expressed interest in the link between nature credits and their NRL obligations, we know that this is not a hypothetical scenario.

Cambodia signals interest in biodiversity credits in its NBSAP - April 13

Cambodia’s updated National Biodiversity Strategy and Action Plan (NBSAP), released in mid-April ahead of COP17, includes language on establishing a government-endorsed biodiversity credit framework. Initial pilots would focus on restoration and a potential credit registry could be integrated with the existing Cambodia Environmental Management Information System (CEMIS). The NBSAP also addresses corporate offsetting, suggesting it should only be used for residual, hard-to-avoid cases of environmental destruction, with offsets prioritizing in-country, like-for-like restoration in priority corridors.

Cambodia is the third Southeast Asian country in three months to signal serious interest in biodiversity credits, after the Philippines reef pilot in February and Thailand’s national roadmap in March. The region is clearly moving with government-led initiatives that could create the regulatory clarity private buyers need before committing capital. Restricting offsets to residual impacts with strict conditions would set a high integrity bar and, if done well, enable another important source of demand.

Market news

CreditNature and Stabiliti partner to embed biodiversity credits into consumer transactions - April 7

CreditNature announced a partnership with Stabiliti, a technology company building infrastructure to route micro-contributions from commercial transactions into verified nature restoration projects. The mechanism works through a configurable “Green Margin” that businesses embed into their products or financial flows, directing a small portion of each transaction toward restoration projects measured under CreditNature’s NARIA framework. Contributions first fund Nature Investment Certificates and eventually generate Nature Credits once ecosystem uplift is verified.

It feels very similar to the Wilderlands x al.ive body case I highlighted last month, where an Australian personal care brand bundled a biodiversity credit with each product sold. The difference is that Stabiliti is trying to build the infrastructure layer that makes this repeatable across sectors, rather than requiring each developer to negotiate individual brand partnerships. I wrote last month that the path of bundling credits into existing purchasing decisions deserves more exploration, and CreditNature seems to agree.

The Landbanking Group prepares to launch European nature cadastre for land-level environmental data - March 30

The Landbanking Group (TLG) is building what it calls a “Cadastre”, a public land registry that tracks the environmental condition of individual parcels of land across biodiversity, carbon, water, and soil indicators. Co-CEO Martin Stuchtey described it as “a digital ecological twin of an entire country”. The pilot of the shared dataset is planned for the end of June, starting in Germany and covering up to 100,000 hectares, with ambitions to scale across Europe.

If a shared, trusted land data layer can reduce the cost of baselining and monitoring, it hits at exactly the right point in the value chain, when projects are in the “death zone” with everything to pay and nothing to earn. I would be curious to see a collaboration between TLG and green account.

Earthly and Nattergal partner to sell biodiversity credits from Boothby Wildland - April 9

Nattergal and Earthly announced a partnership to bring third-party verified biodiversity credits to market from Nattergal’s flagship site, Boothby Wildland in Lincolnshire. The 617-hectare site is being restored from ecologically degraded agricultural land into a mix of wetlands, grasslands, scrub, and woodland, including a beaver reintroduction. Boothby was assessed using Earthly’s Keystone 3.0 framework.

Readers of last month’s edition will recognize the name. Boothby was one of the two sites used in the University of Cambridge study testing the Wallacea Trust‘s biodiversity credit methodology, which found that restoration costs would be roughly fifteen times higher than the credit revenue the site could generate. The Cambridge team concluded that biodiversity credits alone would not fund nature recovery and should be one layer in a blended finance stack. Aligned with this logic, it seems that Boothby Wildland will bundle carbon and biodiversity.

European Investment Fund backs €200m biodiversity private credit fund with €60m guarantee - April 3

The European Investment Fund (EIF), part of the EIB Group, announced a €60 million guarantee to Sienna Investment Managers‘ Biodiversity Private Credit Fund, covering up to 70% of the credit risk on loans to small and medium-sized firms working on biodiversity projects. The fund is classified as Article 9 under the EU’s SFDR and targets a total size of €200 million, with an initial €100 million commitment already secured from French institutional investor Malakoff Humanis Group. The guarantee is backed by the InvestEU Sustainability Guarantee and specifically targets earlier-stage projects with weak collateral.

Most biodiversity credit projects can’t access traditional bank financing because lenders don’t know what to do with them. A public guarantee that absorbs 70% of the credit risk for lenders could be a game-changer in providing the bridge financing that they need between the start of the on-the-ground work and the first credit revenues. We assume the fund would target such projects, but this is not a guaranteed scenario.

New Zealand’s state farmer Pāmu explores biodiversity credits as a revenue stream - April 24

Pāmu, New Zealand’s state-owned farming enterprise, is working with the Ministry for Primary Industries and the Ministry for the Environment on assessing the relevance of biodiversity credits for their operations. Head of sustainability Sam Bridgman told Farmers Weekly that local and international businesses want to buy products or operate in voluntary nature markets tied to good biodiversity outcomes, either for product claims or direct investment. Pāmu currently protects 11,000 hectares across 58 of its 112 farms under QEII covenants and uses environmental DNA testing through Wilderlab to track native species across its properties.

New Zealand is the second-largest VBM market by transaction volume in our database, and the buyer pattern there is almost entirely domestic, with NZ companies buying from NZ projects. The country’s companies are buying voluntary credits, so demand might not be a problem in this case. If Pāmu moves forward, it would be the largest single landowner entering the NZ biodiversity credit market.

Nature Impact acquires third habitat bank site for BNG and voluntary biodiversity credits - April 30

Nature Impact acquired a 41-hectare site in Wrotham, Kent, that will generate both compliance biodiversity net gain (BNG) units and voluntary nature credits. The site, financed by Triodos Bank UK, will be restored from degraded farmland into permanently protected habitats. This is Nature Impact’s third habitat bank across Kent and East Sussex, following a £725,000 loan from Triodos in December 2024 for the first two sites.

Nature Impact taps into the relatively stable BNG market while also producing voluntary credits from the same restoration work. A practical answer to the funding gap that every developer faces, since the compliance market provides the baseline economics (Triodos might not have lent against voluntary credits alone), while voluntary credits make it bankable if some parts are not eligible for BNG. If more developers follow this model in countries with both compliance and voluntary mechanisms, the voluntary market gets to grow with existing infrastructure rather than having to justify its entire economic case from scratch.

Suggested reads

Scaling biodiversity markets

The European Investment Bank (EIB), CDC Biodiversité, and PwC Luxembourg published a major study analyzing what it would take for French corporates and financial institutions to actually buy voluntary biodiversity certificates. Based on interviews and surveys with 37 French ESG and finance executives, the report identifies four persistent barriers: no clear link between certificates and broader policy frameworks like the EU Nature Restoration Law, lack of standardized metrics, no established financial return, and insufficient market size and credibility.

It then delivers six operational recommendations for European policymakers, including creating an EU-wide quality label for biodiversity certificates, establishing regional hubs and a clearing house to match buyers and sellers, introducing mandatory purchase obligations for high-impact sectors, and designing financial incentives like tax credits and public guarantees to improve investment returns.

We provided the market data section of the report, presenting our global VBM transaction analysis (cumulative sales, geographic breakdown, buyer profiles, seller concentration, pricing trends…). I had the chance to present alongside Sabine Bourdy (European Commission, DG ENV), Audrey Coreau (CGDD, French Ministry), Camille Maclet (IAPB), and Jérôme Beilin (Removall Carbon) at the launch event at the Banque de France.

The recommendation on market infrastructure with regional hubs and clearing houses matches what we see in the data: 96% of B2B market value is domestic, transactions don’t cross borders yet, and buyers overwhelmingly prefer local projects. Building market infrastructure that doubles down on this hyper-local reality and enables cross-border liquidity over time seems like the right sequencing.

A behavioural perspective on nature credit markets

The European Commission’s Joint Research Centre (JRC) published a scoping literature review analyzing why motivated actors still don’t participate in nature credit markets, using a behavioural framework (COM-B) that looks at capability, opportunity, and motivation across buyers, suppliers, public authorities, and communities.

The core finding is that financial motivation alone rarely drives participation, and often doesn’t translate into action when structural conditions are misaligned. The report sets regulatory uncertainty, reputational risk, high transaction costs, and unclear risk allocation as the main barriers, and finds strong convergence across both demand and supply actors on two enabling conditions, which are stable policy frameworks and trusted intermediaries.

Companies won’t buy if the end product (credits) is not clear, well-explained, and verified (or at least verifiable) by a trusted party. Intermediaries can help, and I’m not saying that only because we kind of are one. According to the report, intermediaries are seen as trust-building and risk-reducing by both sides of the market. Overall, very interesting reading for anyone working on EU nature credit market design, and directly informs the work the EU Expert Group is doing right now.

Upcoming events

May 11 - “Make Nature Count” seminar and workshop - Norway

Morning seminar at KPMG Oslo exploring how nature can be valued as an economic resource, organized by KPMG, Fossagrim, Gjensidige, and Belief Group. Speakers include Per Espen Stoknes (BI Center for Sustainability), Thina Saltvedt (Nordea Bank), and Dominik Maczik (BCA). The seminar will be followed by an afternoon workshop on building a high-integrity nature market in a European context.

I will attend the event and discuss the state of the market during the workshop. If you plan to attend or will be in Oslo around this day and want to discuss, reach out to me at martin@bloomlabs.earth

Nature Tech Week - May 11-16 - London and Cambridge, UK

The annual gathering of the global nature tech community, running across London and Cambridge. Includes the Nature Action Dialogues hosted by UNEP-WCMC (with sessions from WEF, CDP, WWF, Finance for Biodiversity Foundation, and Cambridge Institute for Sustainability Leadership), and the Nature Tech Unconference where the community sets its own agenda. Satellite events include a biodiversity and nature finance breakfast with IBAT and Conservation International, a Green Finance Institute roundtable, and a rewilding tour at Nattergal’s Boothby Wildland site (which we covered in this edition’s news). Sessions are led by JP Morgan, UNEP-WCMC, Rainforest Alliance, and others.

May 19 - “A Credit to Nature: A Matter of Interest” conference - Belgium

Organized by the Belgian Federal Council for Sustainable Development, with Wageningen University presenting on nature credit market development in the Netherlands, followed by a buyer use-case panel and a lunch marketplace for developers and funders. I love the idea of speed-dating between buyers and sellers, we need more of these.

June 3-4 - EU Green Week 2026 - Belgium

The 26th edition, organized by DG Environment, will be all about the business case for nature. The programme includes a startup-investor matchmaking event for nature-based solutions and nature-related technologies. Simas will attend the event and present the state of the market, so reach out to him at simas@bloomlabs.earth if you want to discuss.

July 14-16 - Global Nature Positive Summit - Japan

An international event to assess the current progress of the Global Biodiversity Framework, under the Japanese Ministry of Environment patronage. If you attend, please reach out to share your findings with us.

October 19-30 - CBD COP17 - Armenia

This is the single most important policy event for VBM in 2026.

| A guest post by

|