It was never really about charity

Skeptics have spent years telling the market that biodiversity credits sell on goodwill, but we might be able to prove otherwise.

Hi, Martin from bloomlabs here.

Welcome to our monthly read of the Voluntary Biodiversity Market (VBM), built on data from our intelligence platform Bloom and the market updates that matter.

For the first time, we took a real look at why companies actually buy biodiversity credits, and we were surprised at how philanthropy is way less important than we thought. On the policy side, 48 countries now name biodiversity credits in their national plans, and much of this month’s news is really governments and institutions getting ready for CBD COP17 in October.

We are also starting a new section this month, Newcomers in Bloom, for the projects and credit schemes that just joined the platform, and it opens with a coral project that arrived with its own film. I got to visit one of the projects we cover too, so a small part of this edition comes from the field.

Explore the data on Bloom.

Market context

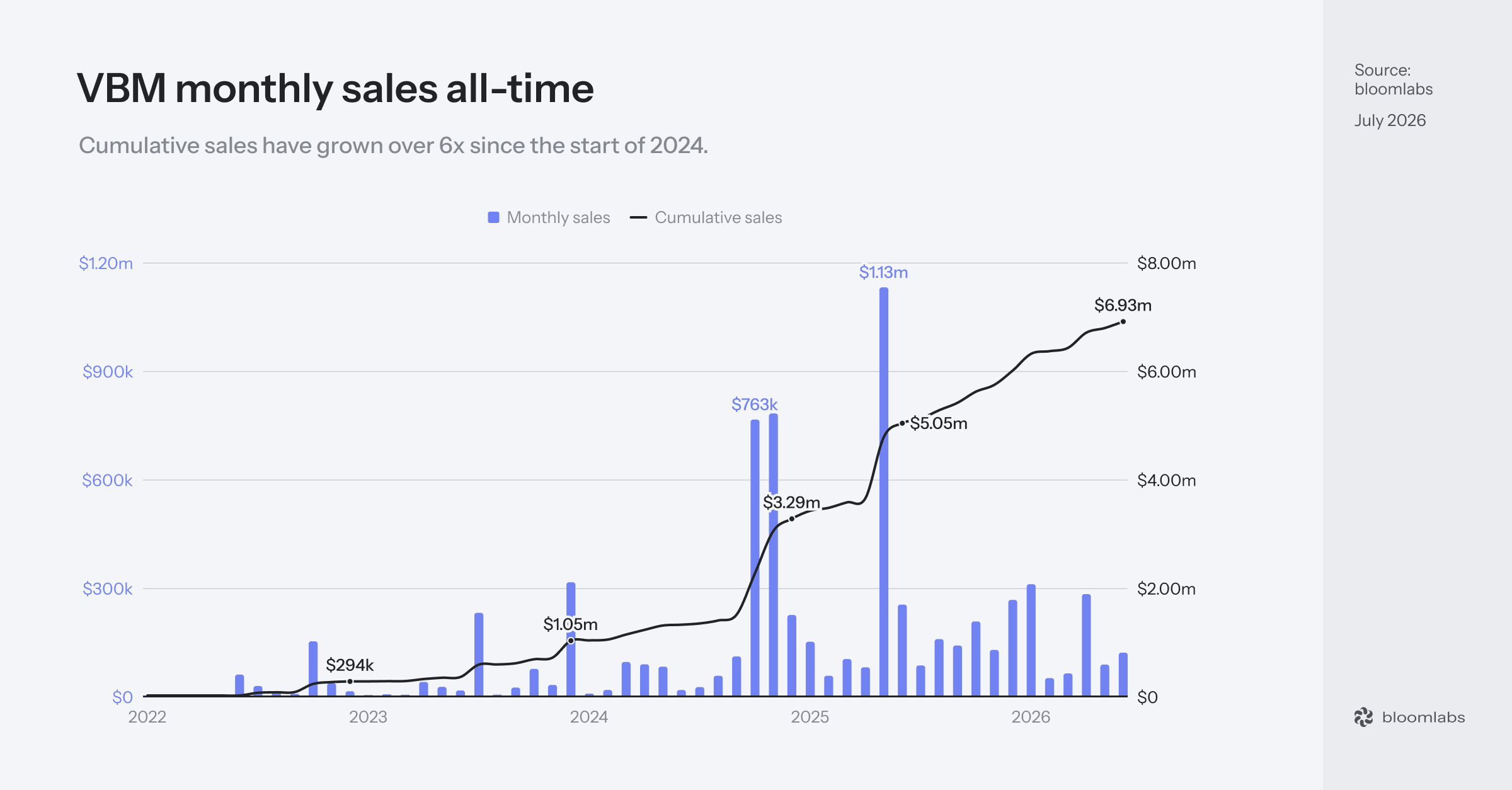

VBM has now sold $6.93m worth of credits since the first recorded sale in early 2022. We still believe a meaningful share of that activity happens over-the-counter and is never announced publicly, which would put the real total somewhere between $8m and $10m.

Volatility is still a thing, with 2026 alone running from $48k in February to $308k in January, and quarterly totals moving from under $100k to nearly $1.8m across the life of the market. June landed at $119k, lifted by a couple of large Australian deals, and it sits well inside that noise. This is why month-on-month or quarter-on-quarter comparisons still do not tell us much.

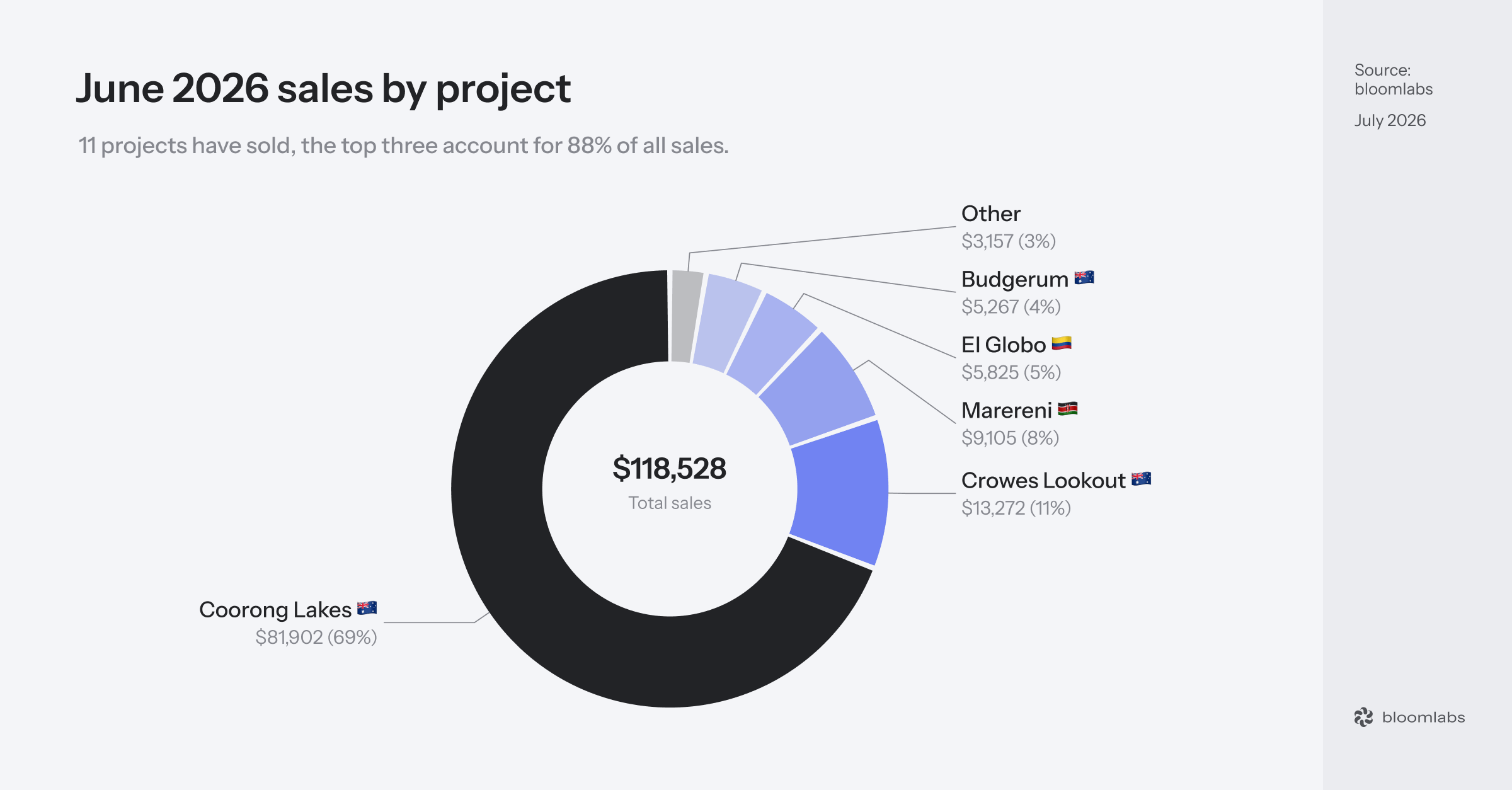

June 2026

June 2026 recorded $119k in sales, up from May’s $85k, across 82 transactions. For comparison, the earlier months of the year came in at $308k in January, $48k in February, $61k in March, $280k in April, and $85k in May. With a median monthly value of $104k since 2024, June sits a little above an average month.

The five largest transactions made up 81% of June’s total, well above May’s 64% and in line with the rest of the year. Two anonymous business purchases of Coorong Lakes credits, worth $40,789 and $31,380, carried 61% of the month between them. Where May was 121 small purchases with no single deal driving it, June was the opposite, carried by those two large deals. The average transaction was worth $1,445, against $706 in May.

Projects

11 projects sold in June, but unlike May, the value was concentrated in one developer and one country. Wilderlands‘ four Australian projects took about 86% of the total, led by Coorong Lakes at $81,902 across 16 transactions, which is 69% of the month on its own. Crowes Lookout added another $13,272, with Budgerum at $5,267 and Alleena at $1,210. Wilderlands regularly sells this mix of a few large B2B deals and a long tail of smaller B2C purchases.

Marereni added $9,105 across 12 transactions of its $3 Kenyan mangrove credits, the kind of steady small volume Seatrees has sold in most months. El Globo in Colombia brought $5,825 across just three transactions, almost all of it from one buyer I will come back to in the next section.

The rest was a long tail of small activity, with the English sites Boothby Wildland, Iford, and Halnaker Hill sold through Earthly adding about $1,844 between them, and the first few dollars landing for one of this month’s newcomers, the coral project Osa Peninsula.

Buyers

Business buyers accounted for 99% of June’s value across just 20 transactions, while consumer buyers made up $1,216 across 62 transactions. That is the usual split, a few business deals carrying the value and a long tail of consumer purchases carrying the count.

Named buyers covered just 6.5% of the value, against 46% in May, because the two large Coorong Lakes purchases and almost all of the other Wilderlands deals came from undisclosed businesses with no country attached. So the single biggest driver of June, Australian Wilderlands credits, ran through buyers we cannot place. However, per our observations of the market so far, it is fair to assume that the majority of those undisclosed buyers are located in the country where the project is based.

The one named buyer interesting to mention is Banco de Occidente, the Colombian bank that first bought El Globo credits in May for $325 and came back in June for $5,775. I flagged the two Latin American banks on El Globo last month as the kind of finance sector interest this market keeps waiting for.

If you are exploring whether and how biodiversity credits fit into your organization’s strategy, we would love to talk, so reach out at hello@bloomlabs.earth.

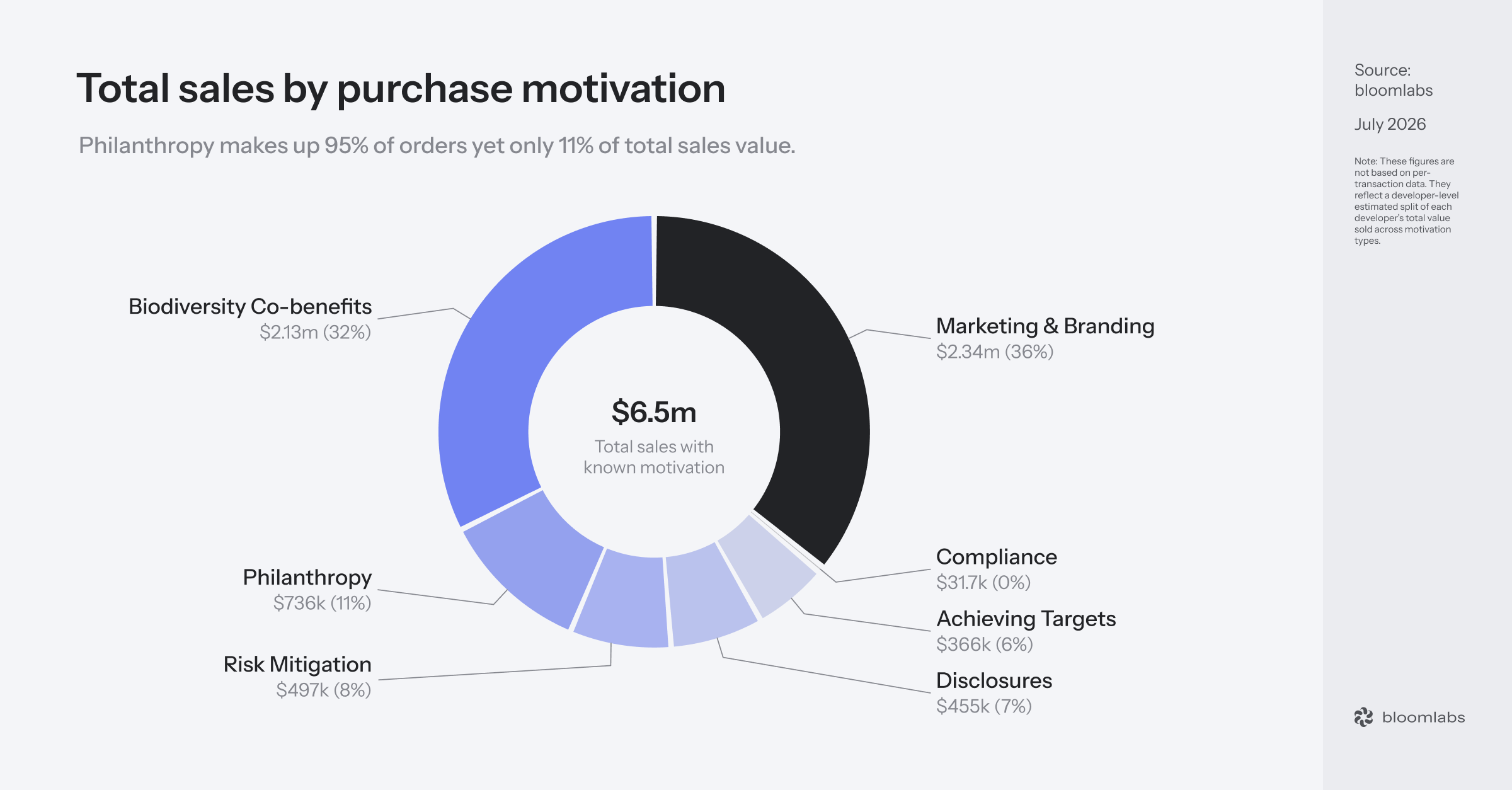

Motivations, rewritten

Skeptics have spent years telling the market that biodiversity credits sell on goodwill, but we might be able to prove otherwise.

We asked the largest developers, who together account for about 95% of all recorded sales, to estimate how their own sales break down across the eight buyer motivations we track. We then weighted each developer’s split by the value they have actually sold and combined them into one market view. This is modeled rather than verified on a deal-by-deal basis, but it is the clearest read of current demand we have.

Marketing and branding leads at 36% of the $6.5m with a known motivation, biodiversity co-benefits sits right behind at 32%, and philanthropy comes a distant third at just 11%.

Two important disclaimers:

The split is self-reported by the developers, who have an obvious incentive to describe their buyers as commercially driven rather than charitable, so the marketing and branding share especially should be read as a direction rather than a hard figure.

While our data tags a number of buyers this way, we can rarely point to one that publicly used biodiversity credits in its marketing, so this motivation shows up in what developers report far more than in anything visible on the ground.

Biodiversity co-benefits are still attached to the carbon market, since most of that money comes from buyers adding a quantified, unitized biodiversity claim to a carbon purchase rather than choosing biodiversity for its own sake.

The motivations that point to more structured, durable demand are no longer a rounding error. Risk mitigation, disclosures, and achieving corporate targets now come to 8%, 7%, and 6%, about a fifth of the value between them, which is more than a market running purely on goodwill would produce.

Demand today runs mostly on reputation and on carbon co-benefits, with early pressure starting to build from risk, disclosure, and targets. The two hardest pulls, a legal obligation to compensate and the expectation of a financial return, are still absent from the purchases we actually see. Philanthropy was always too simple a story, and we are glad to nuance this narrative with new data.

Newcomers in Bloom

Projects

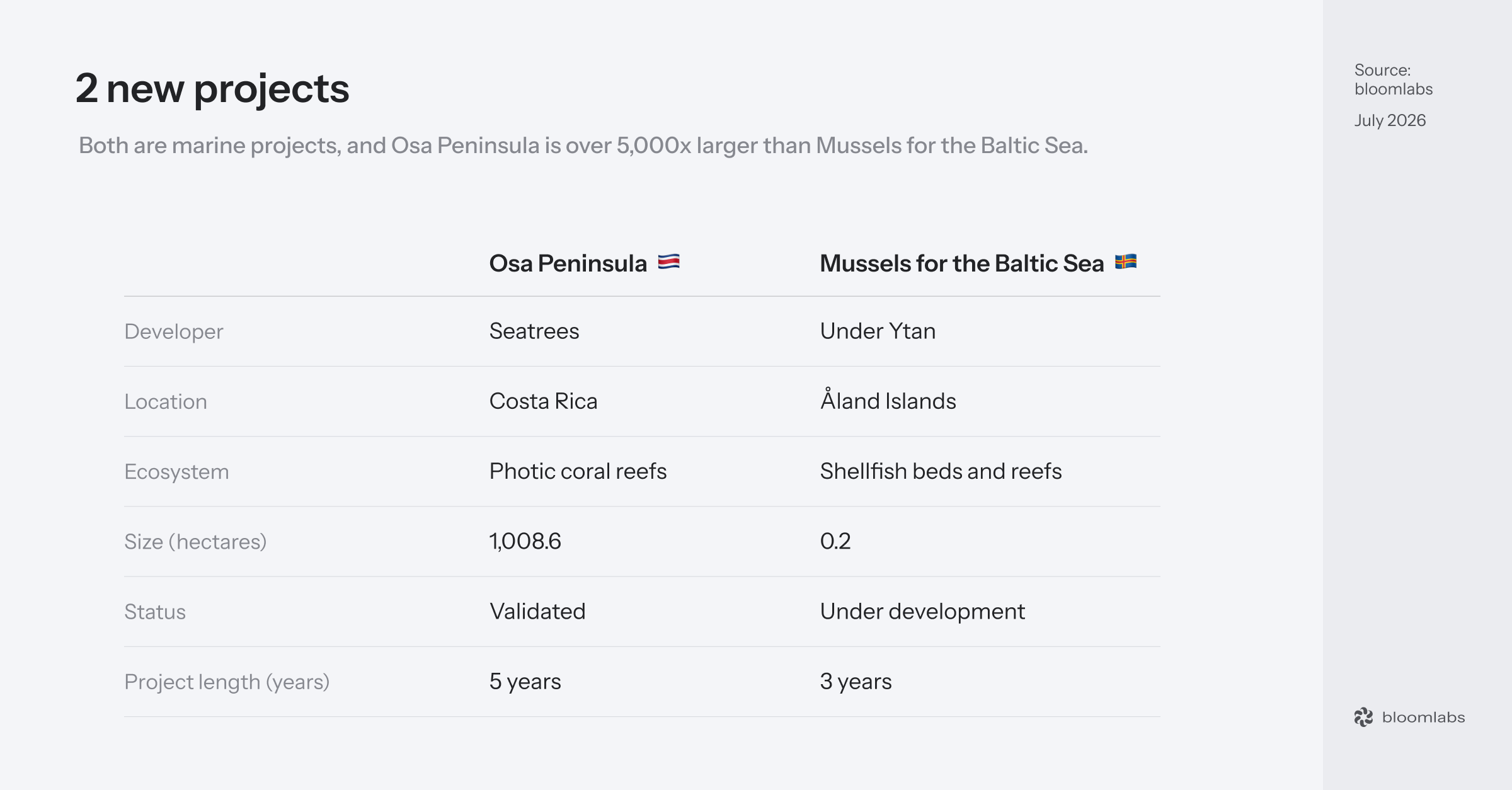

Osa Peninsula

Osa Peninsula is a coral reef restoration project across two sites off Costa Rica’s southern Pacific coast, Golfo Dulce and the reefs around Caño Island, developed by Seatrees with the Costa Rican nonprofit Raising Coral. Over five years, it will plant 4,000 heat-tolerant corals taken from colonies that survived past bleaching, mounted on elevated structures that lift them clear of the sediment.

Each surviving coral and the stewardship around it becomes one Biodiversity Block validated through Regen Network and issued on its blockchain, for 4,000 credits and a target biodiversity uplift of 34.6% across the two sites. Seatrees paired the launch with a beautiful documentary, Symbiosis, which is the first film I know of to make biodiversity credits its main subject. That is why it leads this section, since a market this young has to be explained to people before it can sell to them.

Mussels for the Baltic Sea

Mussels for the Baltic Sea is a pilot in the Åland archipelago from Under Ytan, a local marine restoration company, building rafts of locally sourced material to grow reef-like communities of native blue mussels. The Baltic is one of the most eutrophic seas in the world, where decades of nitrogen and phosphorus runoff have fed algal blooms and oxygen-starved dead zones that land-based controls have not fixed. Mussels help on two fronts at once, since they filter those nutrients out of the water and, once harvested, physically remove the nitrogen and phosphorus, while the structures they colonize lift local species richness.

Schemes

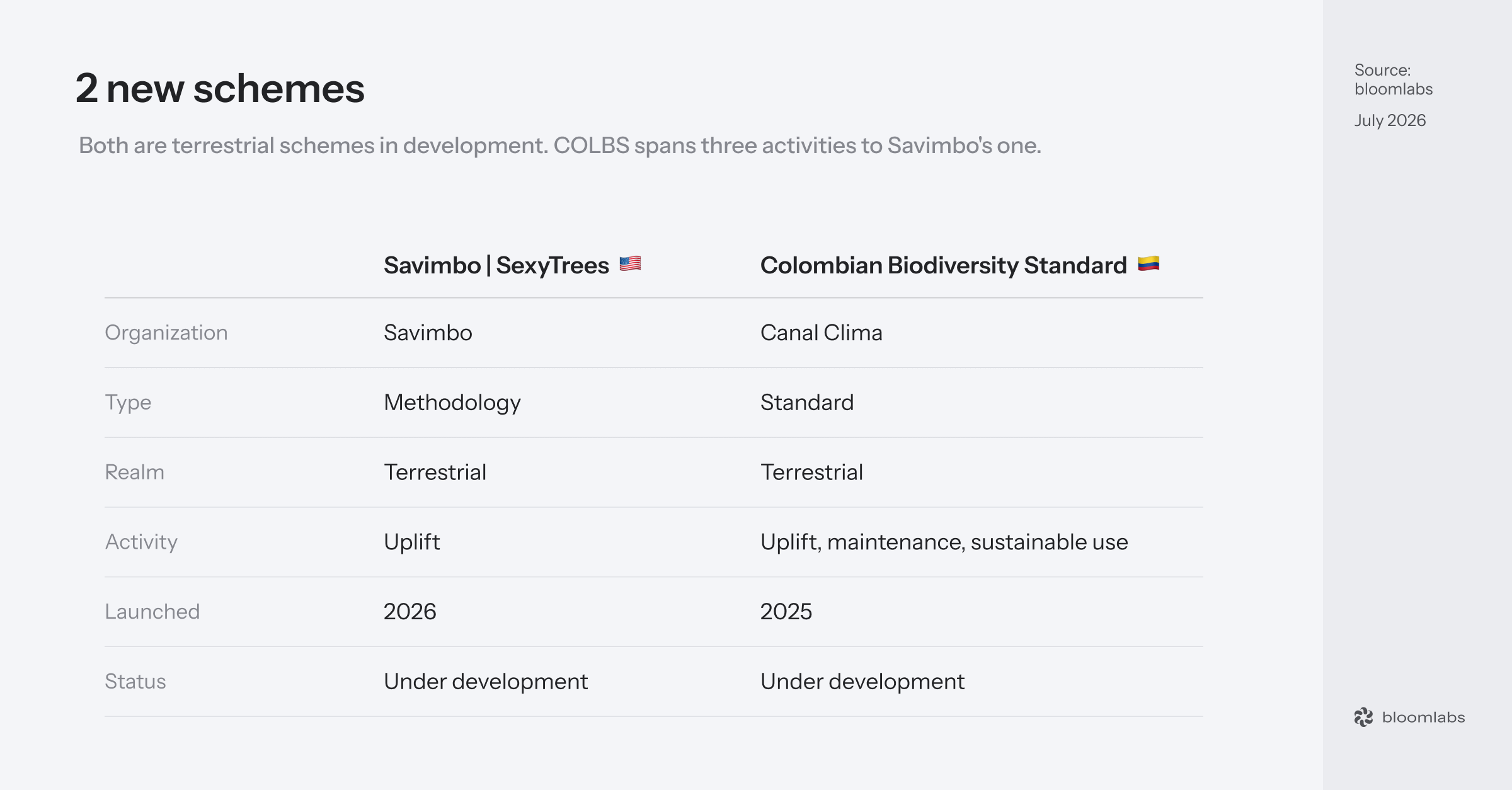

Savimbo | SexyTrees

Savimbo | SexyTrees is an outcome-based restoration methodology published this year by Savimbo, the Indigenous-led developer that is one of the leaders in this market. It works at one-hectare smallholder scale and pays farmers cash for verified tree survival, to restore degraded tropical land through agroforestry. Rather than merge everything into one blended unit, it keeps carbon (trees and biochar), biodiversity, water, and agrobiodiversity as separate credit types stacked on the same hectare, which Savimbo expanded specifically so the layers stack without double counting. The biodiversity layer, measured through eDNA and still labeled experimental, is built to produce the same biodiversity unit as Savimbo’s existing methodology rather than replace it, so one parcel can carry several of these credits at once.

Colombian Biodiversity Standard (COLBS)

Colombian Biodiversity Standard (COLBS) is a certification standard from Canal Clima, a climate and biodiversity company in Bogotá. It is written for both voluntary and regulated use, with its projects bound to be registered through the BioTrust registry. Canal Clima also runs a carbon credit exchange, which puts it in the same camp as the carbon players moving into biodiversity that we keep writing about.

News

Featured

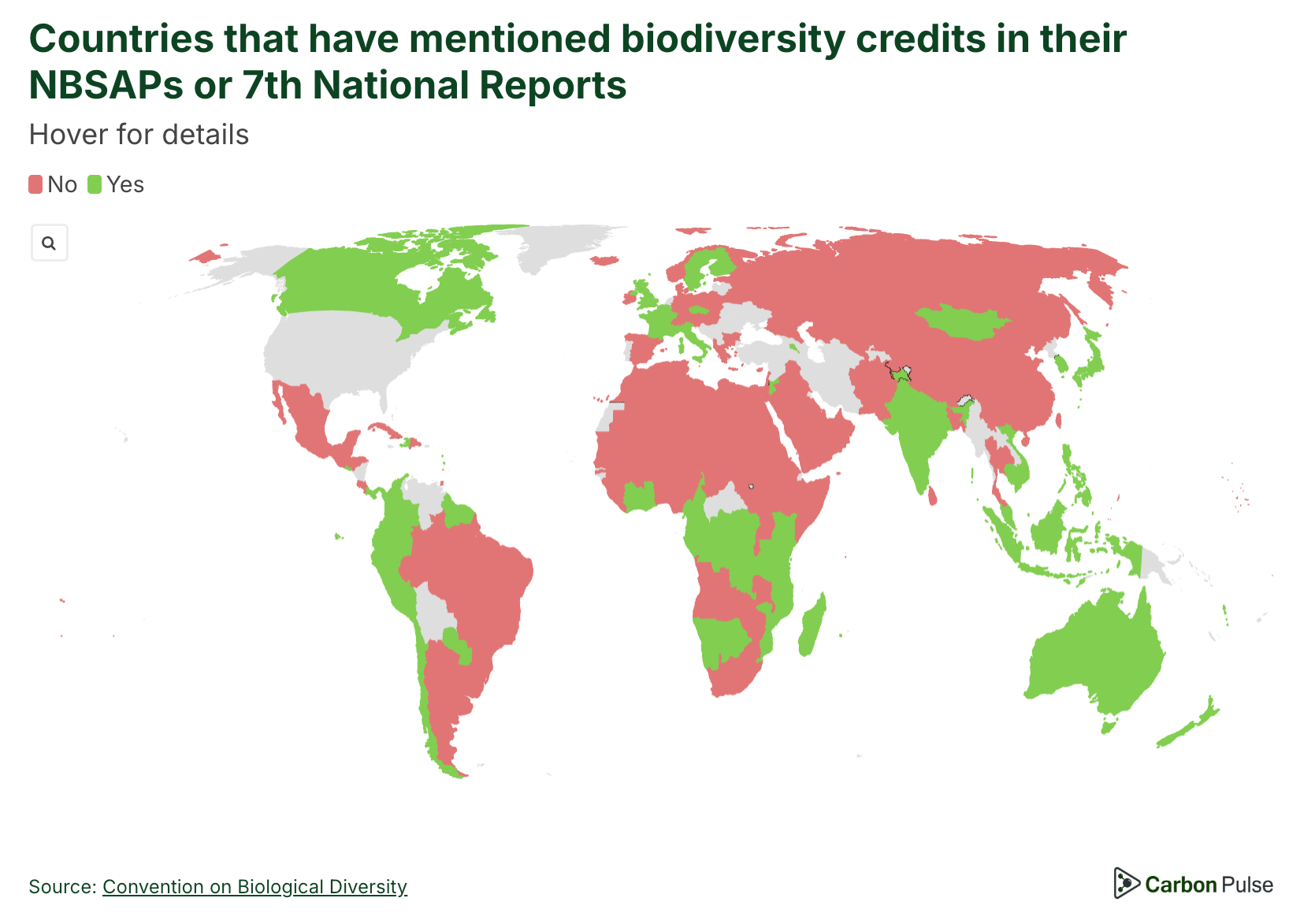

48 countries now name biodiversity credits in their national plans

NBSAP biodiversity credit mentions by country, from CarbonPulse.

CarbonPulse published an analysis on June 18 finding that at least 48 countries reference biodiversity credits in their National Biodiversity Strategies and Action Plans (NBSAP) or their 7th National Reports to the UN, drawn from its new Biodiversity Portal. The mentions concentrate in Europe, the Middle East and Africa with 25 countries, then Asia Pacific with 12 and the Americas with 11, and they exclude anything tied only to compliance offset markets. Finland, Italy, France and Sweden gave clear support, a belt of African states from Gabon to Tanzania named the instruments, and the EU pointed again to its own nature credits roadmap.

Just like we identified Ethiopia and Cambodia in April, this map confirms real interest from a growing share of countries. For now, recognition in national plans is running ahead of actual sales, which is usually the order these things take, since a plan that names an instrument tends to come before a rule that requires it. If voluntary demand stays thin, that is the path by which it could eventually become an obligation, the same mechanism already at work in England’s BNG and German Ökopunkte, even if it takes a few years.

National news

Indonesia and UNDP open a biodiversity credit pilot in Sumatra

On June 8, UNDP’s BIOFIN initiative and the Indonesian government opened a call for one organization to design and pilot a community-level biodiversity credit scheme in Jambi province, on Sumatra, funded with up to $60,000 and running to May 2027. It sits inside a larger effort, since Indonesia is building three biodiversity credit schemes in parallel, a mandatory conservation scheme, a biodiversity offset scheme and a voluntary one, coordinated by a taskforce set up in February.

Indonesia is the country we have flagged most this year, and running mandatory, offset and voluntary tracks at once is rare. The offset and mandatory parts are what matters most for demand, because a legal obligation to compensate creates buyers who do not act on goodwill, the same mechanism we keep pointing to with England’s BNG and Germany’s Ökopunkte.

The Bank of Lithuania measures the biodiversity footprint of its financial sector

At its climate risk forum on June 10, the Bank of Lithuania presented its first assessment of the climate and nature impact of everything its banks, insurers and pension funds finance. It applied two standard metrics, mean species abundance (MSA) and the potentially disappeared fraction of species (PDF) to measure biodiversity impact. On those measures, the corporate bonds and equities held at the end of 2025 map to a complete loss of biodiversity across roughly 15 square kilometers, and to about 236 species lost worldwide over a century if the financed companies never change. That impact is strikingly concentrated, since 98% of it comes from 200 issuers that are only about 5% of the portfolio by value.

What has been missing from voluntary biodiversity demand is a hard reason for companies to act. A central bank quantifying how much nature loss sits inside its financial system is one way to build that reason. Lithuania joins a small group of central banks putting numbers on finance’s nature footprint, and the two metrics it used are the same ones the credit market is trying to standardize around. Supervisory attention can lead to disclosure requirements, and they then generate demand.

Market news

A French developer sells biodiversity, carbon, water and soil credits from the same land

Racines de France is selling credits across four dimensions from the Arches Castriotes project, certified under the Nat5 standard. The units run from €30 for a water credit to €200 for a soil credit, with biodiversity at €80 for 100m2 preserved or restored. It is considered the first project worldwide to obtain the quadruple certification.

This one is a bit special to me, since I was invited to visit it a couple of weeks ago. The project is very well implemented, and the team is dead serious about making it work.

Private capital funds a verified nature recovery project in Yorkshire

CreditNature has put an independently measured forecast behind Broughton Sanctuary, a 607-hectare estate in Yorkshire that four partners are restoring from degraded farmland into woodland, wetland, meadow and moorland. Its Ecosystem Condition Index, a 0 to 100 score that folds four ecological indicators into one measure of landscape health, was measured at 23 at the end of 2025 and is forecast to reach 47 over ten years, generating 150,000 credits. The four partners each own a different link in the same chain, with the estate holding the land and leading the restoration, Ecosulis designing the ecology and running the field surveys, CreditNature measuring and certifying the outcome, and Rebalance Earth committing the working capital up front.

This is the clearest blueprint of what it takes to make voluntary nature markets work so far: large, structured, long-term agreements with a clear division of risk, responsibilities and modeled multi-source cashflows. Congratulations to the partners behind this transaction, you have set an example to follow.

3Bee raises corporate funding for 330 hectares of European biodiversity projects

The Italian developer secured corporate financing for around 330 hectares of voluntary biodiversity credit pilots across Europe, mostly Italy plus Spain and France, with companies paying between €5,000 and €10,000 per hectare per year toward certification under a new Italian standard, UNI/PdR 179.

Its COO Simone Mazzola is clear about the strategy: it is naive to expect companies to invest out of the blue, and without compliance or demand requirements this stays a push market where he convinces buyers one at a time. This is the demand problem we keep pointing at, put plainly by someone who is actually selling the credits. Legal obligations or incentives are what turn interest into durable demand.

Plan Vivo sets out principles for stacking biodiversity and carbon credits

Plan Vivo, the UK standard setter, published a position statement on June 5 on how projects should stack biodiversity and carbon credits. It already allows stacking its PV Nature certificates with its PV Climate carbon credits, and its conditions come down to:

each unit is sold separately with distinct claims

the carbon credit can be used for offsetting, the biodiversity unit cannot

Stacked projects are a realistic first use case for biodiversity credits, because a carbon project that already sells credits can add a biodiversity unit without starting from zero. We argued this in our carbon and biodiversity credits in practice piece, and the projects that actually sell are usually the ones stacking a second revenue stream, such as Wilderlands or Seatrees.

If you are a project developer and wonder how you can use biodiversity credit to combine them to other credits and increase your revenues, we would love to talk. Reach out at hello@bloomlabs.earth.

The Biodiversity Credit Alliance opens its marine principles for feedback

On June 18, the Biodiversity Credit Alliance opened consultation on an issue paper that applies its high-level principles for biodiversity credits to the ocean, drafted by its Marine Biodiversity Credits Working Group. The Great Barrier Reef Foundation and the Global Fund for Coral Reefs introduced it, and the Association for Coastal Ecosystem Services presented the Vanga Seagrass Project in Kenya as a live test of the principles.

Marine biodiversity credits are two to three years behind terrestrial ones. The ocean breaks the physics that land credits lean on, from shifting baselines to unclear rights over a stretch of sea. But BCA’s principles are being checked against a real project, and should lead to the kind of milestone paper they usually produce.

The EU funds IUCN to test nature credits in three member states

IUCN launched an EU-funded project on June 2 to help Croatia, the Netherlands and Poland work out whether nature credits could finance biodiversity restoration, running to October 2027 and feeding the European Commission’s Expert Group on Nature Credits, the same body my co-founder Simas sat with in Brussels in March. It will assess existing metrics and methodologies, design a financing mechanism, and recommend how to govern these credits. The EU keeps running national experiments in parallel with its central policy work. I’m curious to see if and how these initiatives will play a part in the union’s positioning at CBD COP17.

Société Générale puts €100 million into an Ardian nature fund

Société Générale committed €100 million, around $115 million, to Averrhoa NBS, a nature-based solutions fund run by Ardian, and will also act as its financial advisor. The Article 9 fund invests in reforestation and the restoration of wetlands and mangroves, targeting up to 85 million tonnes of carbon over 40 years with biodiversity as a co-benefit. One of Europe’s largest banks committing this budget to nature restoration, and taking the financial advisor role rather than only the investor one, is a real signal that mainstream finance is starting to build nature into its core business.

Upcoming events

Global Nature Positive Summit 2026 - July 14-16 - Kumamoto, Japan

The second edition of the summit, after Sydney in 2024, hosted in Kumamoto under the patronage of the Japanese Ministry of Environment and organized by the Nature Positive Initiative with the IUCN Japan Committee and ICLEI Japan. It focuses on private sector and local government action to deliver the Global Biodiversity Framework, and it is the natural place to watch the state of nature metrics mature, since Japan has more than 200 TNFD adopters and several of the metric pilot companies will be there. If you attend, please reach out to share your findings with us.

CBD SBSTTA 28 and SBI 7 - July 27 to August 12 - Nairobi, Kenya

The two CBD subsidiary bodies meet in Nairobi to prepare the ground for COP17, and biodiversity finance is explicitly on the agenda alongside implementation of the Global Biodiversity Framework. These technical meetings are where the COP17 negotiating text gets shaped, so anything that lands here on finance and resource mobilization is a preview of what the October conference will actually debate. Worth following if you want to read the COP17 tea leaves early.

BIOECON Conference - September 7-8 - Cambridge, UK

A smaller, academic gathering, but very much relevant to VBM this year, with the theme “Economics, Finance and Nature Based Risks” and sessions on conservation instruments and biodiversity economics. If you want the research end of the market, this is where a lot of the thinking that later shows up in methodologies and policy gets argued out first.

Natural Capital Investment Americas - September 15 - New York, US

Environmental Finance’s dedicated natural capital investment conference, timed to sit alongside Climate Week NYC and bringing together investors, asset owners, and regulators.

Climate Week NYC - September 20-27 - New York, US

One of the largest climate events of the year, held alongside the UN General Assembly, with a climate and nature focus area and a thousand-plus affiliated events across the city. As with London in June, the value for our market is less the main stage than the density of nature finance side events and announcements that cluster around it. The World Biodiversity Summit also runs on the sidelines on September 24, though the organizers flag that date as still subject to change.

Building Bridges 2026 - October 6-8 - Geneva, Switzerland

The seventh edition of Geneva’s big sustainable-finance summit, themed around investable solutions, with biodiversity an explicitly welcomed track alongside climate and supply chains. It is a reliably good venue for nature-finance and biodiversity-credit sessions.

CBD COP17 - October 19-30 - Yerevan, Armenia

The single most important policy event for biodiversity credits this year, and the first global review of progress against the Global Biodiversity Framework. Governments will negotiate on resource allocation and finance, which is the track where biodiversity credits sit, so this is the clearest read we will get on where official support for the market actually happens, if it happens at all. More details to come throughout the year.

Le Forum Biodiversité & Économie - November 3-4 - Paris, France

The sixth edition of the French Biodiversity Agency’s biennial forum for business, held at the Cité des sciences et de l’industrie and aimed at companies of every size and sector that want to act on biodiversity.

| A guest post by

|