Monthly Market Overview - May 2026 - New Zealand stole the show

Voluntary Biodiversity Market activity, trends, news, and developments.

Hi, Martin from bloomlabs here.

Welcome to our monthly read of the Voluntary Biodiversity Market (VBM) built on data from our intelligence platform, Bloom and most relevant market updates. New Zealand made the headlines both on policy and sales, and everyone is gearing up for this year’s CBD COP17.

It is also the first edition built on Bloom 2.0, which we just launched. We rebuilt it from the ground up around the “why” behind the “what”: every chart now comes with an analysis paragraph, the data is organized into functional pages (pricing, supply, and demand, interactive world map…). Every dataset has also been expanded and cleaned, now spanning 7,000+ recorded credit sales, 180+ projects and 98 schemes.

Take a look and sign up for free here.

Market context

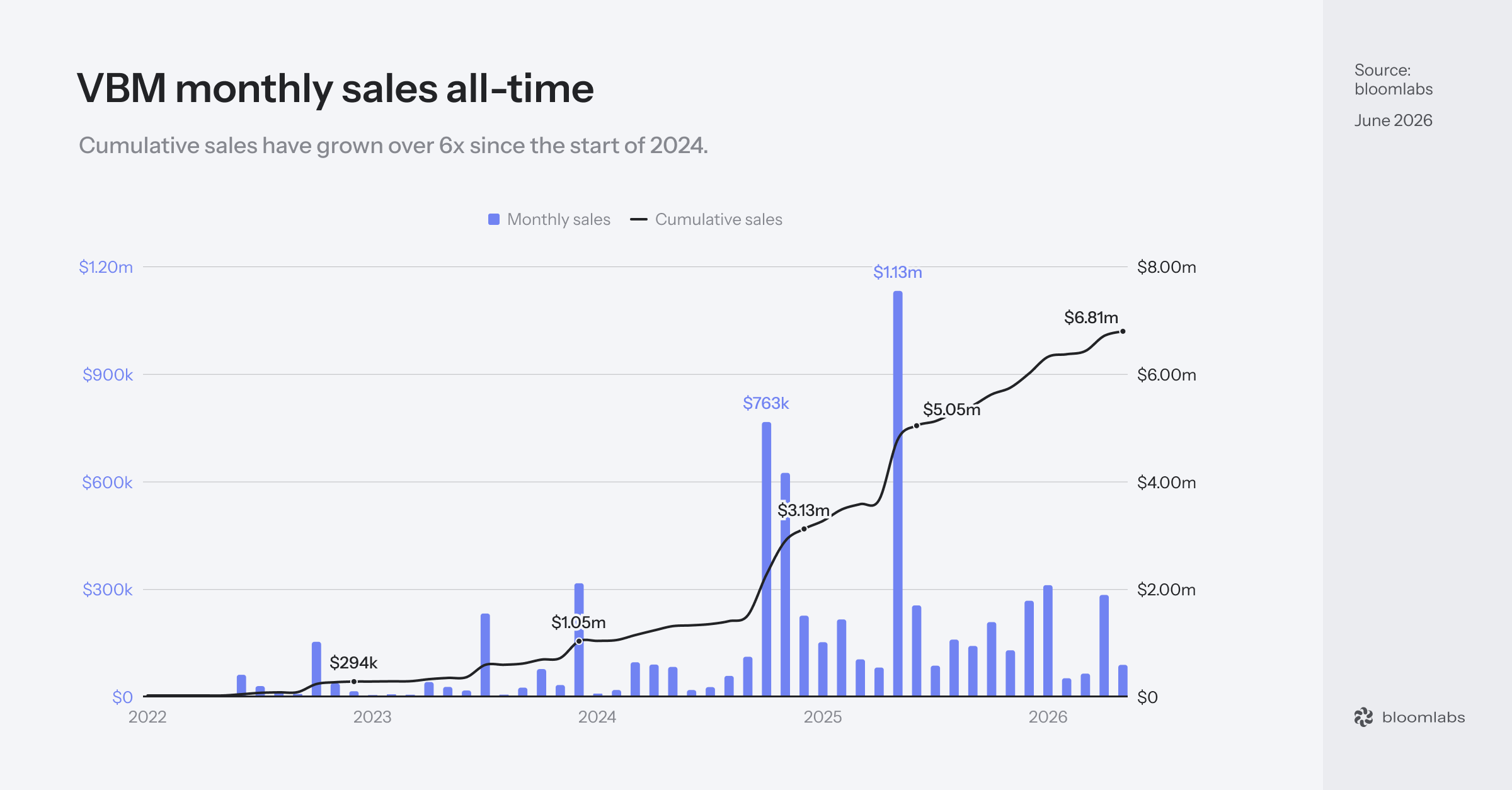

VBM has sold $6.81m worth of credits since the first recorded sale in early 2022. We believe a meaningful share of that activity happened over-the-counter and was never announced publicly, which would put the real total somewhere around $8-10m.

The monthly swings are wide, with 2026 alone running from $48k in February to $308k in January, and quarterly totals have moved between roughly $75k and $1.6m across the life of the market. April was one of those bursts, carried by two German deals, and May is exactly the kind of quiet month that tends to sit around them. This is why month-on-month or quarter-on-quarter comparisons do not tell much yet.

May 2026

May 2026 recorded $85k in sales, down from April’s $280k but with more than twice the number of transactions. For comparison, the previous months came in at $308k in January, $48k in February, $61k in March, and $280k in April. With a median monthly sales value of $84k since 2024, May sits as an average month.

The five largest transactions made up only 64% of May’s total, the lowest share of any month in 2026 (January was 79%, February 82%, March 87%, and April 98%). Where April was one large German burst, May was the opposite, with 121 mostly small purchases and no single deal carrying the month. The average transaction was worth $706, against $5,722 in April.

Projects

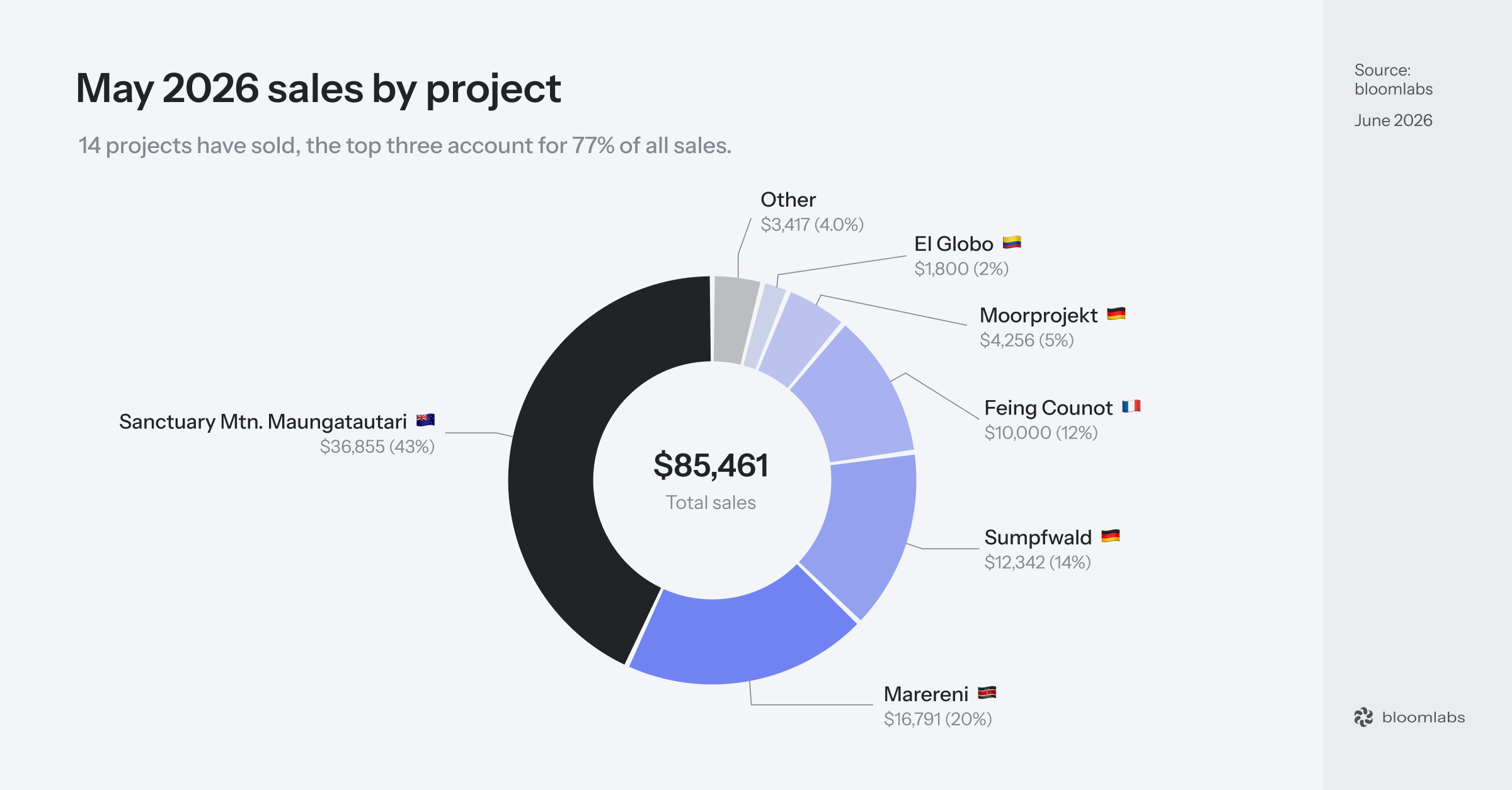

14 projects sold in May, and for once the value was spread across several countries instead of concentrated in one. Sanctuary Mountain Maungatautari led the month with $36,855, which is 43% of the total, across 23 transactions for 5,265 credits at $7 each. It is a fenced New Zealand sanctuary sold through Ekos and its BioCredita programme, and almost all of its value came from named local companies that I will get to in the buyers section.

Marereni came second with $16,791 across 30 transactions, the most of any project this month, selling its $3 Kenyan mangrove credits to a mix of 6 businesses and 24 individuals. Marereni is one of the most reliable sources of demand we track, and Seatrees keeps showing that a relatively cheap and simple unit generates steady volume.

green account, the German marketplace we started tracking earlier this year, carried 21% of this month’s sales, spread across Sumpfwald ($12,342), Moorprojekt ($4,256), and Ippenburg ($1,320). France appeared in the data too, with Feing Counot, a project from Le Printemps des Terres, recording a single $10,000 business purchase for 2,000 credits at $5 each, enough for 12% of the month on its own.

The rest was a long tail of small activity, with El Globo in Colombia at $1,800 across 13 transactions, Wilderlands‘ four Australian projects adding $1,185 between them, and the two Earthly-sold English sites, Iford and Boothby Wildland, contributing $530 and $242.

Buyers

Business buyers accounted for 94% of the value sold, across only 24 transactions, while consumer buyers made up the remaining $5,375 across 97 transactions. This is the pattern we see almost every month, where a small number of business purchases carry the value and a long tail of consumer purchases carries the volume.

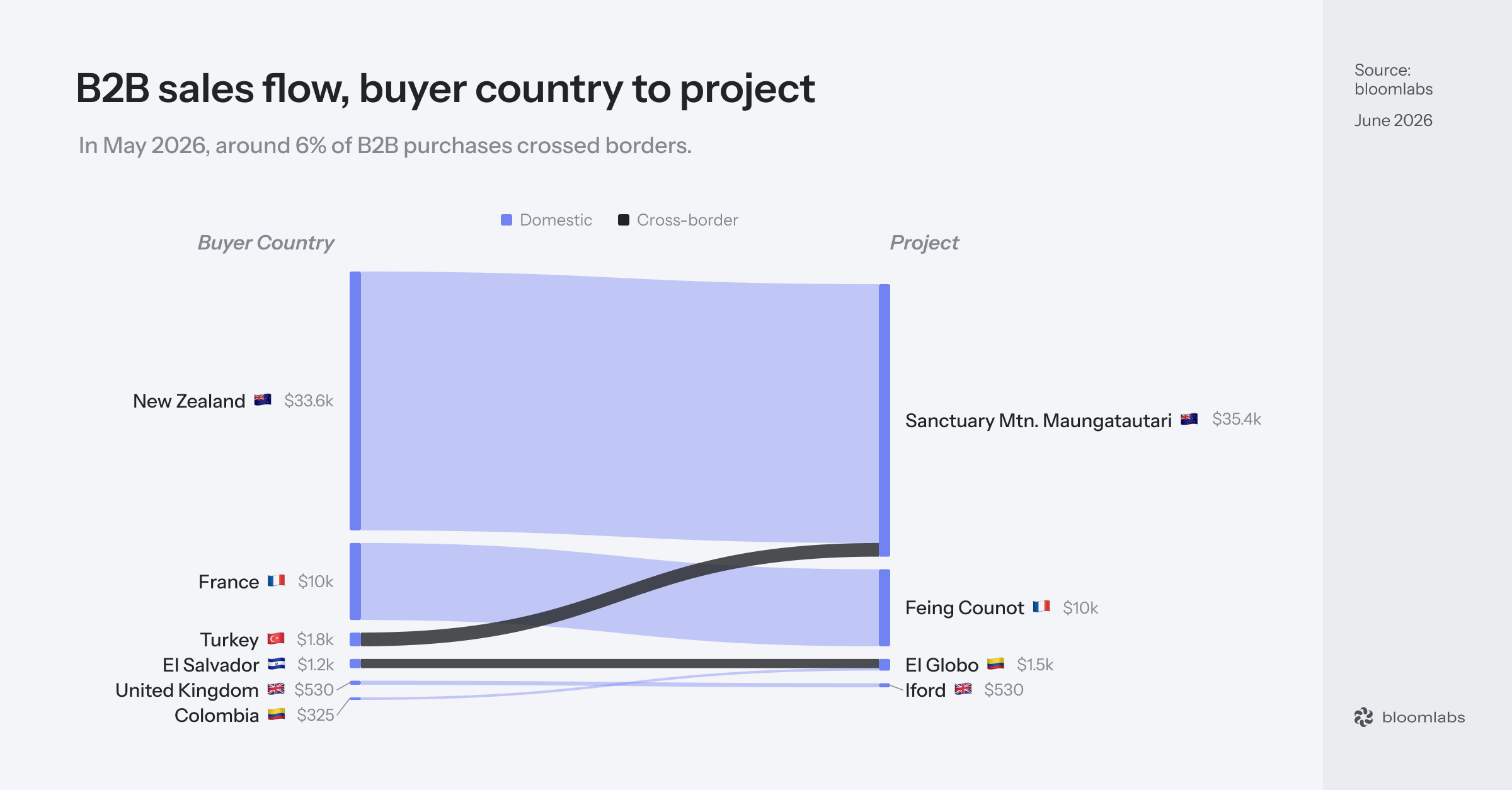

Named buyers covered 46% of May’s value, which is a real improvement on April, when almost everything was anonymous. The biggest was Tonkin + Taylor, the New Zealand engineering and environmental consultancy, which bought $17,066 of Sanctuary Mountain credits and is now a returning buyer after first purchasing in May 2025. Right behind it, Picot Productions, a New Zealand manufacturer, made its first appearance in the data at $10,416, which is a large opening purchase by VBM standards. Most of Sanctuary Mountain’s other buyers were also New Zealand companies, including the New Zealand Educational Institute, The Hello Cup Company, Kimi Ora Resort, Tourism Industry Aotearoa, and Origin Fire Consultants.

This is the same local buyer, local project pattern where New Zealand businesses buy a New Zealand project, mostly in tourism, hospitality, and professional services. The demand is real and it recurs, but it is fully domestic, and that is the part of VBM that still does not behave like an international market.

Two transactions crossed borders though, accounting for 6% of this month’s B2B value. Flamingo Technologies, a Turkish company, bought $1,778 of Sanctuary Mountain credits, and Banco Agrícola of El Salvador bought $1,200 of El Globo credits in Colombia. That second purchase is part of a small but interesting signal, because another Latin American bank, Banco de Occidente, also bought El Globo credits this month. Two banks turning up on the same Colombian project in the same month is the kind of finance-sector interest this market keeps waiting for, even at these small ticket sizes.

If you are exploring whether and how biodiversity credits fit into your organization’s strategy, we would love to talk, so reach out at hello@bloomlabs.earth.

News

Featured: New Zealand builds and unbuilds

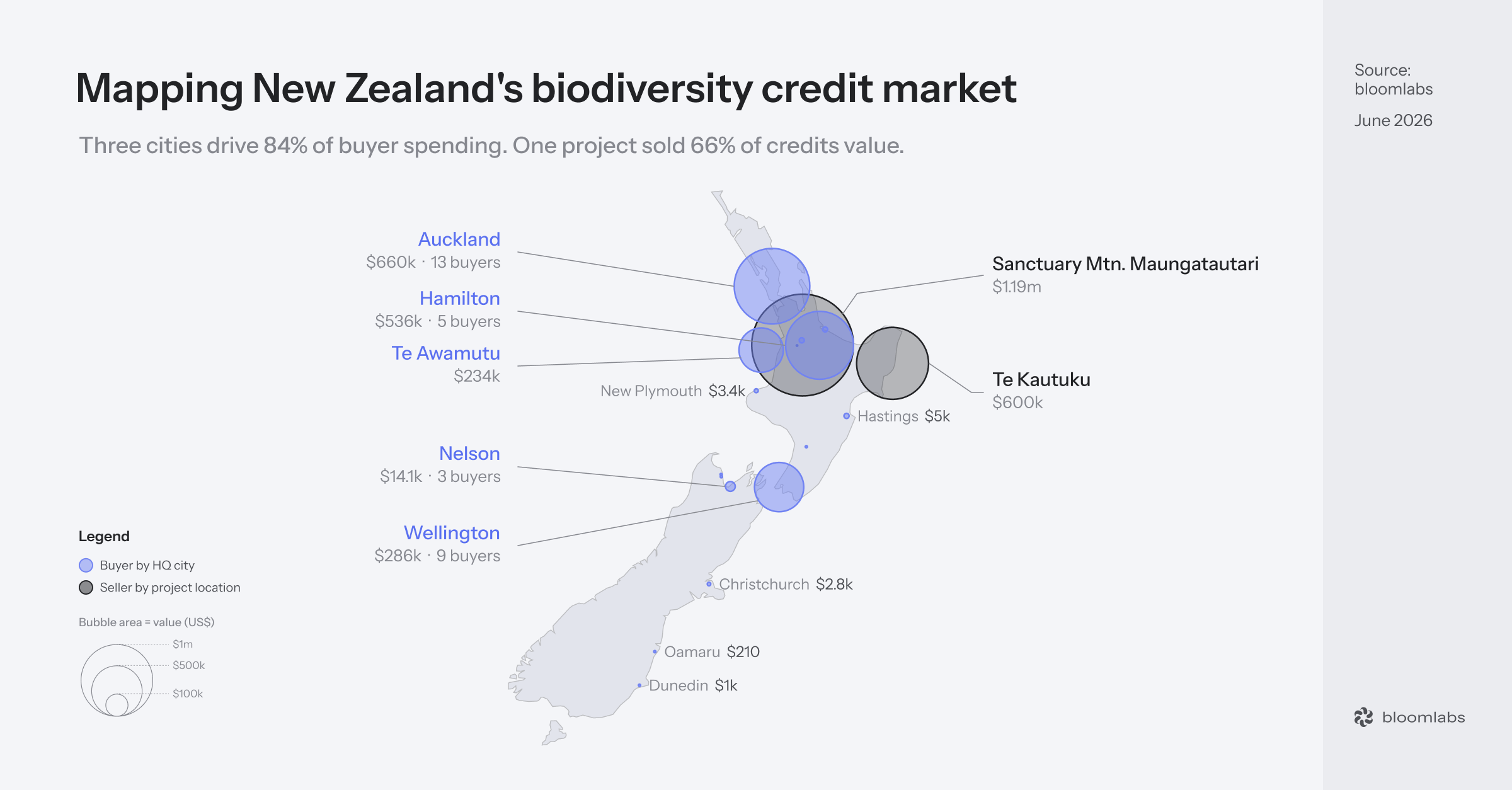

New Zealand had the most consequential month of any country we track, and it pointed in two directions at once.

On May 11, Associate Environment Minister Andrew Hoggard announced a framework to grow voluntary carbon and nature markets. The state will not run the market but will stand behind it through an assurance role Hoggard compared to a “warrant of fitness”, with international schemes already operating in New Zealand recognized from the start and domestic schemes now able to apply for a national endorsement assessed by an independent assurer. Climate Change Minister Simon Watts paired it with refreshed guidance for participants, and the framework also opens public conservation land to privately funded projects.

But opening public conservation land is a contested move. A paper led by Marie Doole of Mataki Environmental in Policy Quarterly warns that voluntary biodiversity credit markets rarely scale and that private money should not replace public conservation funding. She has raised alarms on additionality, because a credit sold to fund work the Crown should already pay for does not add new capital, it replaces another one.

Then the same government moved in the opposite direction. Within about 24 hours it advanced legislation to quash climate activist Mike Smith’s tort case, protecting major emitters, and gave a first reading to what was billed as the biggest overhaul of the Conservation Act in 40 years. Local coverage settled on the line that it was one step forward, three steps back. The markets framework was the rare policy both Federated Farmers and Forest and Bird praised, and it got squeezed between less progressive actions.

In our own May data, the single biggest project was Sanctuary Mountain Maungatautari, and almost every buyer behind it was a New Zealand company, which is exactly the kind of domestic market the government’s new framework is built to support. What complicates the picture is the rest of what the government did the same week. A state stamp of credibility is worth a lot to a very nascent market, but it is worth less coming from a government that is loosening environmental protection with its other hand.

National news

France rebranded its SNCRR sites as “France Crédits Biodiversité”

At the second Roquelaure “entreprises et biodiversité” event in Paris, in front of about 200 business leaders, Minister for Ecological Transition Mathieu Lefèvre announced that France’s natural compensation, restoration and renaturation sites (SNCRR), created in late 2023 under the green industry law, will be renamed “France Crédits Biodiversité.” The target is 30 approved sites by 2030, up from just three approved so far. Lefèvre also confirmed that the accounting standards authority (ANC) is extending its ecological accounting work to biodiversity, with conclusions due in autumn 2026 and large-scale experiments from 2027, and floated a €100 million “Nature” seed fund through France 2030.

A nice rebrand of the mechanism I covered in March, when Removall and CDC Biodiversité signed the first deal to sell SNCRR-certified credits. What I would actually watch is the ANC accounting work, because if France manages to put biodiversity credits into a recognized corporate accounting standard, that does more to create durable demand than any rebrand.

Colombia launched a nature-resilience program using biodiversity credits

The United Nations Development Programme and Colombia’s national parks agency launched a three-year program called “Corredores de Resiliencia” (Resilience Corridors), funded with CAD $6 million from the government of Canada, to reduce the risks of extreme drought in key ecosystems through ecological restoration, wildfire prevention, and nature-based solutions. The program builds local capacity in biodiversity credits, habitat banks, and payments for ecosystem services, aims to restore more than 1,500 hectares, and connects to protected areas including Chingaza and Sumapaz national parks.

Adaptation and disaster-risk money, funded by Canada and run through UNDP, that explicitly treats biodiversity credits and habitat banks as tools to attract longer-term private capital into restoration. It’s a different entry point than the corporate or compliance demand we usually track. Using climate-adaptation finance to prepare the ground for biodiversity credits is a model worth watching in other countries exposed to drought and fire.

Australia consulted on letting Nature Repair certificates supply offsets

The Australian government consulted on policy settings to let biodiversity certificates from its Nature Repair Market be used as environmental offsets. Under last year’s environmental law reforms, the ban on using these certificates for offsetting is expected to lift on December 1, 2026, and a new national Environmental Protection Agency commences July 1. The detail that matters most for developers came out of the consultation, which is that non-offset biodiversity certificates can be stacked with Australian Carbon Credit Units, so a project can sell carbon and biodiversity separately from the same land, while offset-eligible certificates cannot be stacked because the carbon scheme’s additionality rules exclude anything mandated by law.

This is the compliance-pulls-voluntary thesis again, since the moment biodiversity certificates can satisfy a legal offset obligation, you create demand that does not depend on corporate goodwill, the same logic I keep pointing to with England’s BNG and the US mitigation market.

Fiji’s Forestry Act 2025 opened the door to carbon and biodiversity credits

Fiji’s Forestry Act 2025, which replaced a 1992 decree, creates a statutory basis for carbon financing, biodiversity credits, and payments for ecosystem services. The Act requires free, prior and informed consent, clarifies carbon rights for Indigenous iTaukei landowners, and aligns with the EU Deforestation Regulation. Fiji is a small market, so I would not overstate the near-term supply. But it adds to the Pacific and Southeast Asia momentum we have tracked all year.

Thailand’s Doi Tung model moved toward a biodiversity credit scheme

On World Biodiversity Day, the Mae Fah Luang Foundation, through its decades-old Doi Tung development project in Chiang Rai, set out work with Thailand’s environmental policy office and BEDO, the Biodiversity-Based Economy Development Office, to assess the feasibility of using the Terrasos scheme to issue credits, alongside biodiversity baseline data and recognition of conserved areas. This follows Thailand’s national biodiversity credit roadmap through BEDO that we covered in March, so it reads as the same national effort moving from a roadmap into a concrete pilot site with real biodiversity data behind it.

Zimbabwe convened specialists to build a national biodiversity credit framework

Zimbabwe’s Ministry of Environment, Climate and Wildlife held a two-day technical workshop in Kadoma to advance a national biodiversity credit framework, bringing together environmentalists, bioscientists, legal experts, and others around sustainable finance and revenue-sharing for local communities. The ministry set three goals, which are defining what counts as a biodiversity unit, building the monitoring and data systems to back credits with measurable results, and finalizing a draft statutory instrument setting out who can participate, from private landowners to rural communities.

Indonesia pushes biodiversity credits to close funding gap

Indonesia’s national planning ministry, Bappenas, is promoting biodiversity credits as an innovative financing instrument, with three pilot projects and a biodiversity credit white paper underway with UNDP's Biodiversity Finance Initiative (BIOFIN) support. Bappenas sets Indonesia’s national development priorities and feeds into how the budget gets allocated, so it could play a crucial role in how VBM is seen and used in the country.

Market news

The EU lines up nature credits for COP17

With CBD COP17 opening in Yerevan, Armenia on October 19, the European Commission spent late May positioning nature credits as part of what it brings to the table. On May 21 it convened around 100 stakeholders for an event called “Private Biodiversity Financing, From Policy to Portfolio,” and the next day it published two pieces restating how it intends to close the biodiversity financing gap, with nature credits sitting alongside the Nature Restoration Regulation.

None of this is new policy because the underlying Roadmap towards Nature Credits was published back in July 2025. The Commission simply reaffirmed the roadmap and turned it into a pre-COP17 talking point, sending signals about where nature credits sit in the EU’s priorities this year.

The European Commission is also weighing a platform to test whether nature credits generated from different ecosystems, such as wetlands and forests, can be traded and made interoperable, an idea set out by DG Environment policy officer Hadrien Michel during an EU-backed webinar. The platform would sit under Green Assist, the Commission’s advisory program, which is already funding nature credit pilots in France and Estonia and planning more, and Michel said a new advisory project would bring those pilots together to test how tradable and interoperable their credits are, with first results expected by the end of the year.

The Biodiversity Credit Alliance and IAPB pledged to align before COP17

On the International Day for Biological Diversity, the Biodiversity Credit Alliance (BCA) and the International Advisory Panel on Biodiversity Credits (IAPB) issued a joint statement pledging to align their workstreams around shared principles, credible governance, and practical implementation pathways ahead of CBD COP17. The two have been the main standard-bearers for high-integrity biodiversity credits and cohesion between organizations in the market.

Fragmentation between the bodies trying to set the rules has been one of the quieter risks for this market, so two of the most important ones publicly committing to converge before COP17 is a great credibility signal. The COP17 in October will be the moment of truth for institutional trust, so alignment between these two now is crucial.

TNFD, GRI, and SBTN opened a consultation on shared nature metrics

TNFD, GRI, and SBTN released a joint discussion paper on how to fold the Nature Positive Initiative’s state-of-nature metrics into their respective frameworks across assessment, disclosure, transition planning, and target setting. BioInt’s Joshua Berger flagged it as the most concrete convergence moment yet for corporate biodiversity measurement. The NPI metrics come out of a roughly two-year consensus process and a 2025 piloting program across more than 30 organizations.

The three dominant disclosure and target-setting frameworks are now moving to speak one language about the state of nature. A biodiversity credit is only as credible as the metric under it, and if a company’s disclosure, its science-based target, and a credit it buys all rest on the same measures, the whole system gets way more direct, and hence way more usable.

African and Arab states put biodiversity finance on the table in Nairobi

56 countries at the 12th Regional Dialogue on Biodiversity Finance for Africa and the Arab States, held in Nairobi and hosted by the Government of Kenya with UNDP’s Biodiversity Finance Initiative (BIOFIN). The dialogue was framed around moving from designing national biodiversity finance plans to implementing them, against the roughly $700 billion annual global shortfall, and it covered finance solutions including blended finance, green bonds, and biodiversity credits.

Biodiversity credits now seem to show up by default in these regional finance dialogues, sitting in the same toolbox as green bonds and blended finance rather than as an exotic idea. Forty-four African and Arab states have joined BIOFIN since 2024, so a lot of national finance plans are being written right now, and the ones that name credits are the early indicator of where government-backed demand and supply could appear next. That is the same signal I read into the wave of NBSAPs and national roadmaps we have tracked all year.

Capital and demand signals

The UK’s Big Nature Impact Fund hit a £64.6 million first close

The Big Nature Impact Fund, managed by Finance Earth and backed by the UK government, reached a £64.6 million first close, past its initial £50 million target and on the way to a final target of £90-120 million. The private investors, including Zurich, Admiral, the Esmée Fairbairn Foundation, and the Church of England, recover their capital plus a 7% preferred return before the government sees any money back, a structure Finance Earth says turns every £1 of public money into at least £2 of private investment and potentially £3 by the final close. The fund generates revenue by selling carbon credits (Woodland Carbon Code and Peatland Code) and statutory Biodiversity Net Gain units through offtake agreements.

This is the clearest proof yet that institutional money is there when the risk is clearly scoped, and it is the same blended structure I flagged with the European Investment Fund’s guarantee to Sienna in April, where public capital pulls private lenders into nature. Even though not directly related to VBM, this fund makes a perfect example to follow.

The Nature Finance Accelerator launched as a Swiss foundation for nature markets

The Nature Finance Accelerator Foundation is spinning out of the think tank NatureFinance as a Swiss public-benefit foundation, with a planned ten-year mandate to build infrastructure for a high-integrity nature market in Switzerland. It is backed by CHF 7.5 million (about $9.6 million) in catalytic capital and will be run by Henrique Martins, a former climate finance specialist at the UN Environment Programme Finance Initiative. Its work spans nature finance, open-source measurement and verification tools, and what it calls market creation.

This is useful and necessary catalytic philanthropy building the plumbing. Switzerland getting a dedicated vehicle backed by serious money is a good thing, and I will be more interested once it helps move a credit.

Ekko launched a payments tool targeting $1 billion for nature by 2030

London fintech Ekko launched the Nature Footprint, a tool that lets payment providers offer customers the option to support nature projects at checkout, including by rounding up their purchases, with a stated target of channeling up to $1 billion into environmental projects by 2030. It is very similar to the CreditNature and Stabiliti partnership I covered in April. I find the channel genuinely interesting, because consumer payment rails are huge and a tool that plugs into them once and repeats across merchants is a different demand model than the local-buyer-local-project pattern we see in the transaction data every month.

Recommended reads

Demystifying biodiversity finance

The paper published in Nature Reviews Biodiversity by a team from Oxford’s Leverhulme Centre for Nature Recovery (Harrison Carter, Sophus zu Ermgassen, and others), looks at return-seeking biodiversity finance (equity, loans, bonds, carbon credits and biodiversity credits). The big picture: there isn’t enough money going into protecting and restoring nature. The bottom line: these return-seeking tools could help, but only if investors get better returns and lower risk while keeping honest checks on real nature outcomes and fair treatment of local people, and it’s still unclear whether that’s possible at scale. According to the researchers, many nature projects will never attract private money, so government and philanthropic funding will stay essential.

The companion Oxford expert comment, by Carter and zu Ermgassen, makes the same case in plainer language, warning about over-crediting, and noting that more than US$1.1 billion was wiped off the voluntary carbon market’s value in 2023 after over-crediting was exposed. Carter puts the framing as biodiversity finance being “not simply good or bad. It is evolving.”

This is the most useful read of the month for anyone serious about the market, because it asks the harder question, which is whether you can design these instruments to pay investors and deliver real ecological outcomes at the same time. This Oxford group sits behind a lot of the rigorous scrutiny of biodiversity finance right now, including the offsetting paper below.

Read the paper and the Oxford expert comment.

Nature finance: we need (some) offsets

A preprint led by Joseph Bull, argues that biodiversity offsetting has to stay part of the toolkit, even though it should be tightly limited and closely scrutinized, because removing it entirely would leave a real gap in nature finance. Offsets (measures that compensate for negative impacts), are one of the financing tools the Kunming-Montreal Global Biodiversity Framework itself points to, and the paper argues there is no realistic path to the global goal of reversing biodiversity loss without at least some robust offsetting.

I find this a useful counterweight to the view that offsetting is the original sin of nature markets. Bull’s argument is not that offsets are good, it is that they currently fund a meaningful share of conservation and create an incentive to avoid damage in the first place, so banning them without a replacement just removes money and pretends the problem is solved. That said, the whole case rests on offsets being robust and used only as a last resort under the mitigation hierarchy, so I read this as an argument for fixing offsetting rather than a defense of how it usually works today. The debate matters for credits directly, because nature credit standards split on whether they permit offsetting at all.

Upcoming events

London Climate Action Week - June 20-28 - London, UK

One of the largest independent climate gatherings, spread across hundreds of events over nine days, with a dedicated nature cluster sitting alongside the finance and resilience tracks. The main program regularly hosts nature finance and biodiversity credit side events, so if you are in London that week it is a good place to find the people working on this.

Trellis Impact 26 and GreenFin - June 23-25 - San Francisco, US

The combined Trellis event, formerly GreenBiz, spanning decarbonization, nature regeneration, and sustainable finance, with the GreenFin program as its finance pillar. The nature and finance tracks cover natural capital, nature-based solutions, and biodiversity-finance strategies for corporates and investors, which makes it one of the more useful US gatherings for the demand side of this market.

Global Nature Positive Summit 2026 - July 14-16 - Kumamoto, Japan

The second edition of the summit, after Sydney in 2024, hosted in Kumamoto under the patronage of the Japanese Ministry of Environment and organized by the Nature Positive Initiative with the IUCN Japan Committee and ICLEI Japan. It focuses on private sector and local government action to deliver the Global Biodiversity Framework, and it is the natural place to watch the state of nature metrics mature, since Japan has more than 200 TNFD adopters and several of the metric pilot companies will be there. If you attend, please reach out to share your findings with us.

CBD SBSTTA 28 and SBI 7 - July 27 to August 12 - Nairobi, Kenya

The two CBD subsidiary bodies meet in Nairobi to prepare the ground for COP17, and biodiversity finance is explicitly on the agenda alongside implementation of the Global Biodiversity Framework. These technical meetings are where the COP17 negotiating text gets shaped, so anything that lands here on finance and resource mobilization is a preview of what the October conference will actually debate. Worth following if you want to read the COP17 tea leaves early.

BIOECON Conference - September 7-8 - Cambridge, UK

A smaller, academic gathering, but very much relevant to VBM this year, with the theme “Economics, Finance and Nature Based Risks” and sessions on conservation instruments and biodiversity economics. If you want the research end of the market, this is where a lot of the thinking that later shows up in methodologies and policy gets argued out first.

Natural Capital Investment Americas - September 15 - New York, US

Environmental Finance’s dedicated natural capital investment conference, timed to sit alongside Climate Week NYC and bringing together investors, asset owners, and regulators.

Climate Week NYC - September 20-27 - New York, US

One of the largest climate events of the year, held alongside the UN General Assembly, with a climate and nature focus area and a thousand-plus affiliated events across the city. As with London in June, the value for our market is less the main stage than the density of nature finance side events and announcements that cluster around it. The World Biodiversity Summit also runs on the sidelines on September 24, though the organizers flag that date as still subject to change.

Building Bridges 2026 - October 6-8 - Geneva, Switzerland

The seventh edition of Geneva’s big sustainable-finance summit, themed around investable solutions, with biodiversity an explicitly welcomed track alongside climate and supply chains. It is a reliably good venue for nature-finance and biodiversity-credit sessions, and Switzerland’s own nature-market push, including the new Nature Finance Accelerator Foundation I covered in capital signals, gives the 2026 edition some extra local momentum.

CBD COP17 - October 19-30 - Yerevan, Armenia

The single most important policy event for biodiversity credits this year, and the first global review of progress against the Global Biodiversity Framework. Governments will negotiate on resource allocation and finance, which is the track where biodiversity credits sit, so this is the clearest read we will get on where official support for the market actually happens, if it happens at all. More details to come throughout the year.

| A guest post by

|